#分享美股交易赢英伟达股票 June 9 U.S. stock market summary: A waterfall V-shaped reversal during the session, the market waits quietly for CPI to ignite a new direction

June 9, Tuesday, U.S. stocks staged a thrilling deep V rollercoaster. The three major indices experienced a programmatic, panic-driven plunge at one point, with the Nasdaq dropping as much as 3.6%, but in the afternoon, bullish funds vigorously bottom-fished, successfully recovering most of the losses by the close.

In one sentence: The Dow Jones closed at 50,872.11 +0.17%, affected by intra-day panic, but resilient cyclicals performed strongly, turning positive in the late session. The S&P 500 closed at 7,386.65 -0.26%, rebounded in the morning to test the monthly line but faced resistance, then broke below the 30-day moving average during the session, triggering a sell-off, but was strongly pulled back at the end. The Nasdaq closed at 25,678.82 -0.97%, with tech stocks and AI hardware sectors facing intense selling pressure during the day; after a deep V rebound, it still closed slightly lower by 1%.

Sector overview: Technology sector retreated, optical communication sector plummeted.

The key market information summary is as follows: CPI data for May is about to be released. The market generally expects that rising oil prices may cause overall CPI to be somewhat hot, but core CPI will be relatively moderate. Bullish funds tend to believe that a “bad news is already priced in” trend may emerge tomorrow night.

Additionally, next week’s Bank of Japan rate hike is already a certainty, and the Federal Reserve’s policy meeting on June 17 is viewed as this month’s most critical liquidity watershed.

Geopolitical tensions once again amplify market volatility. The Chief of Staff of the Israeli Defense Forces stated that they are ready to resume operations against Iran at any time, followed by Trump tweeting that U.S. helicopters were attacked and emphasizing the need to respond. Trump’s unpredictable remarks shattered previous peace negotiation expectations, directly causing algorithmic trading and panic selling to surge, leading to liquidity fragmentation.

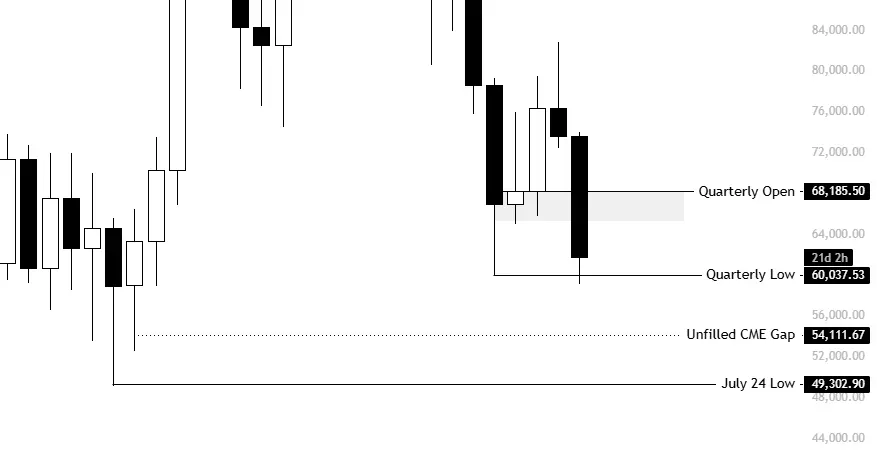

Key levels for commodities and crude oil: Brent crude oscillates widely around $100, with multiple attempts to surpass $110 forming 3 to 4 peaks. Currently, $90 is the last line of defense; a sudden break below $90 would constitute a technical breakdown. Industry and sector updates: Philadelphia Semiconductor Index fell 1.93%, with the daily candlestick reaching and closing at the 30-day moving average. Market risk appetite shows a short-term directional shift. Some funds are taking profits from high positions in AI hardware and semiconductor sectors and withdrawing.

As the World Cup approaches, hot money begins flowing into traditional consumer and gambling concept stocks, pushing related stocks to rise against the trend; influenced by the Energy Department’s signal of increased crude oil transportation, oil prices have retreated, suppressing inflation expectations, and U.S. Treasury yields have retraced from high levels. Leading AI hardware and optical module giants briefly fell below the 50-day moving average to around $200 during the session, then were pulled back by funds after clearing many stop-loss orders. The optical module leader faced profit-taking due to circulating rumors of “next-generation upgrade technology delays,” while another large AI company saw its co-founder and institutional shareholders cash out billions of dollars, raising market concerns about its financial health and high debt levels.

Technology and computing stocks

Apple (AAPL) played the “Air Force One” of the day, leading the sell-off, but ultimately closed with a lower shadow on the daily candlestick;

GigaTech (GBL) surged pre-market after a social media influencer publicly praised its 1.6T pluggable optical module business; AI applications and software sectors (like Wei Lao Ba) performed extremely weakly, showing a reverse-market streak of consecutive declines, with funds following the decline rather than the rise.

Microsoft declined during the market rebound, fell more sharply during the big drop, and continued to lag during the V-shaped reversal, becoming the worst performer among the seven giants since the beginning of the year. Microsoft experienced 7 consecutive declines, with a year-to-date drop of 16% (even worse than Tesla’s 11% decline).

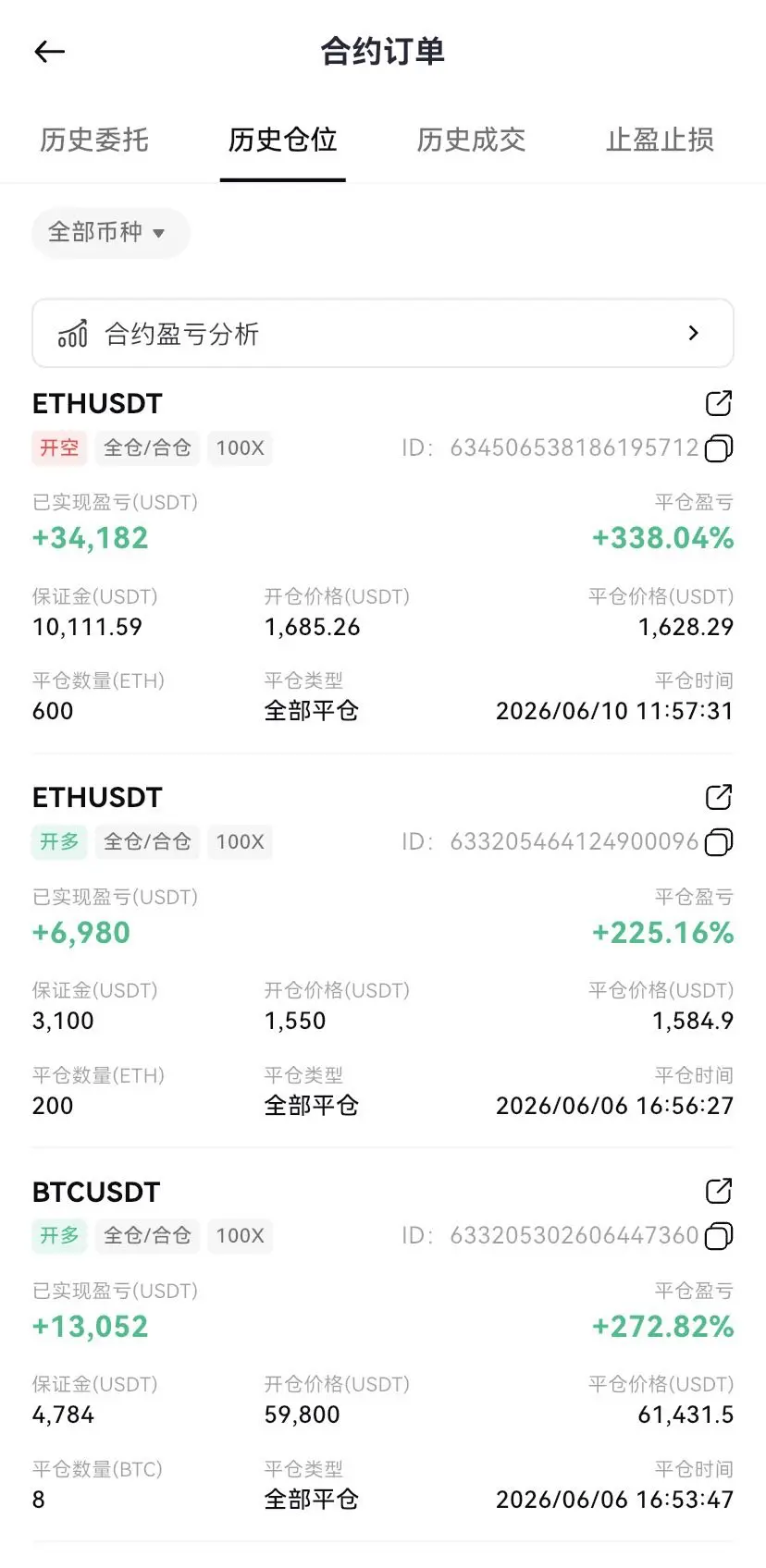

Space stocks (e.g., W) launched a $500 million ATM equity issuance plan, causing a sharp drop in stock price, indicating that under SpaceX’s integrated advantage, secondary market commercial space concept stocks are being heavily squeezed in valuation premiums, with funds rapidly concentrating on top players.

Focus on tonight’s CPI data and Oracle’s earnings report; currently, U.S. stocks are not looking optimistic, and the semiconductor hardware sector remains high-risk.

June 9, Tuesday, U.S. stocks staged a thrilling deep V rollercoaster. The three major indices experienced a programmatic, panic-driven plunge at one point, with the Nasdaq dropping as much as 3.6%, but in the afternoon, bullish funds vigorously bottom-fished, successfully recovering most of the losses by the close.

In one sentence: The Dow Jones closed at 50,872.11 +0.17%, affected by intra-day panic, but resilient cyclicals performed strongly, turning positive in the late session. The S&P 500 closed at 7,386.65 -0.26%, rebounded in the morning to test the monthly line but faced resistance, then broke below the 30-day moving average during the session, triggering a sell-off, but was strongly pulled back at the end. The Nasdaq closed at 25,678.82 -0.97%, with tech stocks and AI hardware sectors facing intense selling pressure during the day; after a deep V rebound, it still closed slightly lower by 1%.

Sector overview: Technology sector retreated, optical communication sector plummeted.

The key market information summary is as follows: CPI data for May is about to be released. The market generally expects that rising oil prices may cause overall CPI to be somewhat hot, but core CPI will be relatively moderate. Bullish funds tend to believe that a “bad news is already priced in” trend may emerge tomorrow night.

Additionally, next week’s Bank of Japan rate hike is already a certainty, and the Federal Reserve’s policy meeting on June 17 is viewed as this month’s most critical liquidity watershed.

Geopolitical tensions once again amplify market volatility. The Chief of Staff of the Israeli Defense Forces stated that they are ready to resume operations against Iran at any time, followed by Trump tweeting that U.S. helicopters were attacked and emphasizing the need to respond. Trump’s unpredictable remarks shattered previous peace negotiation expectations, directly causing algorithmic trading and panic selling to surge, leading to liquidity fragmentation.

Key levels for commodities and crude oil: Brent crude oscillates widely around $100, with multiple attempts to surpass $110 forming 3 to 4 peaks. Currently, $90 is the last line of defense; a sudden break below $90 would constitute a technical breakdown. Industry and sector updates: Philadelphia Semiconductor Index fell 1.93%, with the daily candlestick reaching and closing at the 30-day moving average. Market risk appetite shows a short-term directional shift. Some funds are taking profits from high positions in AI hardware and semiconductor sectors and withdrawing.

As the World Cup approaches, hot money begins flowing into traditional consumer and gambling concept stocks, pushing related stocks to rise against the trend; influenced by the Energy Department’s signal of increased crude oil transportation, oil prices have retreated, suppressing inflation expectations, and U.S. Treasury yields have retraced from high levels. Leading AI hardware and optical module giants briefly fell below the 50-day moving average to around $200 during the session, then were pulled back by funds after clearing many stop-loss orders. The optical module leader faced profit-taking due to circulating rumors of “next-generation upgrade technology delays,” while another large AI company saw its co-founder and institutional shareholders cash out billions of dollars, raising market concerns about its financial health and high debt levels.

Technology and computing stocks

Apple (AAPL) played the “Air Force One” of the day, leading the sell-off, but ultimately closed with a lower shadow on the daily candlestick;

GigaTech (GBL) surged pre-market after a social media influencer publicly praised its 1.6T pluggable optical module business; AI applications and software sectors (like Wei Lao Ba) performed extremely weakly, showing a reverse-market streak of consecutive declines, with funds following the decline rather than the rise.

Microsoft declined during the market rebound, fell more sharply during the big drop, and continued to lag during the V-shaped reversal, becoming the worst performer among the seven giants since the beginning of the year. Microsoft experienced 7 consecutive declines, with a year-to-date drop of 16% (even worse than Tesla’s 11% decline).

Space stocks (e.g., W) launched a $500 million ATM equity issuance plan, causing a sharp drop in stock price, indicating that under SpaceX’s integrated advantage, secondary market commercial space concept stocks are being heavily squeezed in valuation premiums, with funds rapidly concentrating on top players.

Focus on tonight’s CPI data and Oracle’s earnings report; currently, U.S. stocks are not looking optimistic, and the semiconductor hardware sector remains high-risk.