#AIChipStocksSurgeMicronLeadsGains

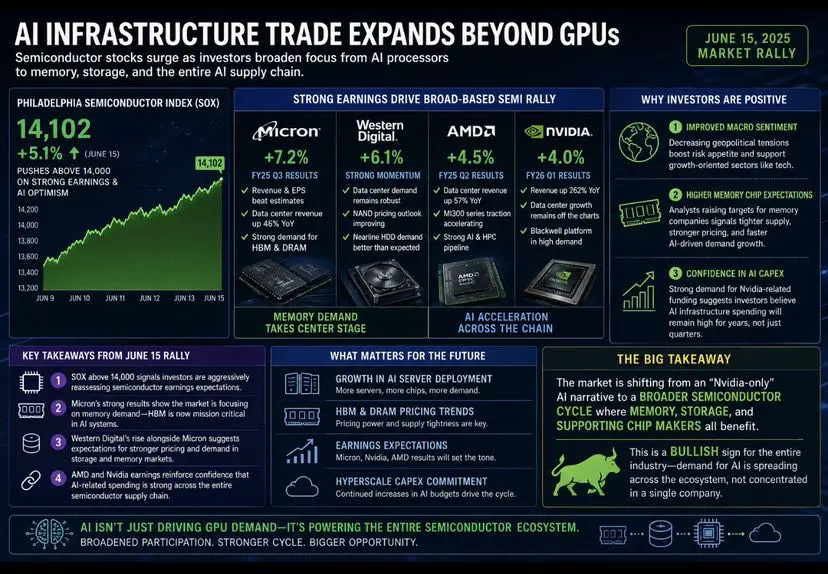

This move reflects a classic “AI infrastructure trade” expanding beyond just GPU manufacturers.

Key takeaways from the June 15 rally:

* The Philadelphia Semiconductor Index rising above 14,000 indicates investors are aggressively reassessing semiconductor earnings expectations.

* Leading earnings from Micron Technology show the market is increasingly focusing on memory demand rather than just AI processors. High-bandwidth memory has become a critical component in AI systems.

* Western Digital’s rise alongside Micron suggests investors expect stronger pricing and demand in the storage and memory markets.

* Earnings from Advanced Micro Devices and Nvidia demonstrate confidence that AI-related spending remains strong across the entire semiconductor supply chain.

Reasons for the positive investor reaction:

1. Improved macroeconomic sentiment

* Decreasing geopolitical tensions generally boost risk appetite and support growth-oriented sectors like technology.

2. Higher Memory Chip Expectations

* If analysts significantly raise their targets for memory companies, this usually signals expectations of tighter supply, stronger pricing, and faster AI-driven demand growth.

3. Confidence in AI Capital Spending

* Strong demand for Nvidia-related funding can be interpreted as investors believing that AI infrastructure spending will remain high for years rather than just quarters.

What Matters for the Future

The sustainability of the uptrend will depend on:

* Growth in AI server deployment.

* HBM and DRAM pricing trends.

* Earnings expectations from Micron, Nvidia, and AMD.

* Whether hyperscale cloud providers will continue to increase their AI spending budgets.

A key takeaway is that the market appears to be shifting from an "Nvidia-only" focused AI narrative to a broader semiconductor cycle where memory, storage, and supporting chip manufacturers also benefit. This is generally a bullish sign for the entire industry, as it indicates that demand for AI is spreading across the ecosystem rather than being concentrated in a single company.

This move reflects a classic “AI infrastructure trade” expanding beyond just GPU manufacturers.

Key takeaways from the June 15 rally:

* The Philadelphia Semiconductor Index rising above 14,000 indicates investors are aggressively reassessing semiconductor earnings expectations.

* Leading earnings from Micron Technology show the market is increasingly focusing on memory demand rather than just AI processors. High-bandwidth memory has become a critical component in AI systems.

* Western Digital’s rise alongside Micron suggests investors expect stronger pricing and demand in the storage and memory markets.

* Earnings from Advanced Micro Devices and Nvidia demonstrate confidence that AI-related spending remains strong across the entire semiconductor supply chain.

Reasons for the positive investor reaction:

1. Improved macroeconomic sentiment

* Decreasing geopolitical tensions generally boost risk appetite and support growth-oriented sectors like technology.

2. Higher Memory Chip Expectations

* If analysts significantly raise their targets for memory companies, this usually signals expectations of tighter supply, stronger pricing, and faster AI-driven demand growth.

3. Confidence in AI Capital Spending

* Strong demand for Nvidia-related funding can be interpreted as investors believing that AI infrastructure spending will remain high for years rather than just quarters.

What Matters for the Future

The sustainability of the uptrend will depend on:

* Growth in AI server deployment.

* HBM and DRAM pricing trends.

* Earnings expectations from Micron, Nvidia, and AMD.

* Whether hyperscale cloud providers will continue to increase their AI spending budgets.

A key takeaway is that the market appears to be shifting from an "Nvidia-only" focused AI narrative to a broader semiconductor cycle where memory, storage, and supporting chip manufacturers also benefit. This is generally a bullish sign for the entire industry, as it indicates that demand for AI is spreading across the ecosystem rather than being concentrated in a single company.