#WeakNFPShakesRateHikeOdds

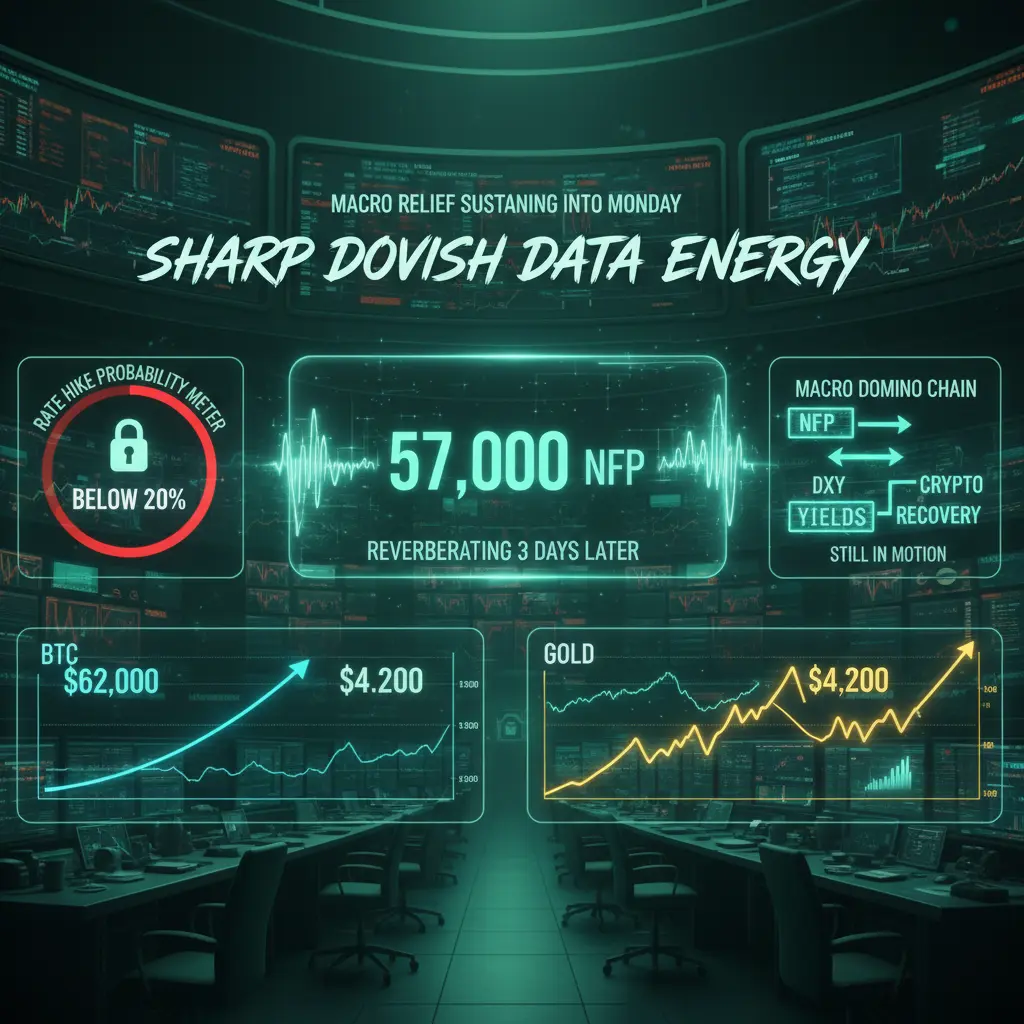

The cryptocurrency market has staged a meaningful recovery after the weaker-than-expected June Non-Farm Payrolls (NFP) report reduced expectations for another Federal Reserve rate hike. The softer labor data weakened the U.S. dollar, improved overall market liquidity, and boosted demand for both digital assets and traditional safe havens such as gold.

Although the recovery has been impressive, investors should recognize that the rally has been driven by a combination of improving macroeconomic sentiment, aggressive short covering, and renewed speculative activity rather than broad institutional accumulation.

This distinction will determine whether the current move evolves into a sustainable uptrend or remains a temporary relief rally.

Bitcoin (BTC): Institutional Recovery with Cautious Optimism

Bitcoin has recovered from approximately 57,000 USD to around 62,850 USD, representing a gain of more than 10 percent from recent lows. Weekly performance has improved to roughly 5.15 percent, while daily gains continue to hold near 1 percent, confirming renewed buying momentum.

Trading activity remains exceptionally healthy.

The BTC/USDT pair on Gate has recorded hundreds of millions of dollars in daily trading volume, demonstrating that this recovery is supported by genuine market participation rather than thin liquidity.

Bitcoin's market capitalization has recovered to nearly 1.24 trillion USD, while U.S. Spot Bitcoin ETFs ended a prolonged outflow streak with approximately 224 million USD of fresh inflows.

Nevertheless, cumulative institutional flows over the previous month remain deeply negative at approximately 6.27 billion USD, suggesting that large investors continue to approach the market cautiously.

Derivative markets remain balanced with neutral funding rates and steadily rising open interest.

Options positioning, however, continues to favor downside protection, indicating that professional traders are maintaining defensive hedges despite recent price appreciation.

Solana (SOL): The Strongest Large-Cap Performer

Solana has emerged as the strongest performer among major cryptocurrencies.

SOL has gained nearly 18.6 percent during the past week, significantly outperforming Bitcoin and most leading digital assets. The network now carries a market capitalization approaching 47 billion USD while maintaining one of the highest growth rates among Layer-1 ecosystems.

One of the primary catalysts behind Solana's strength has been the explosive expansion of tokenized equity trading. Daily trading activity surrounding tokenized stocks has increased dramatically, generating billions of dollars in network volume and attracting fresh liquidity into the ecosystem.

Perpetual futures trading also reflects elevated investor participation, with Solana recording substantially higher derivatives volume than many competing large-cap cryptocurrencies.

This combination of growing ecosystem activity, institutional attention, and increasing liquidity continues to position Solana as one of the highest-beta assets during improving market conditions.

XRP: Stable Institutional Demand Continues

XRP has also participated strongly in the broader recovery.

The asset has appreciated approximately 10 percent over the week while maintaining healthy daily trading volume above 1.5 billion USD.

XRP's market capitalization remains near 70 billion USD, supported by growing institutional adoption and improving regulatory clarity.

Unlike Solana, XRP's performance is driven less by speculative momentum and more by payment infrastructure adoption and long-term institutional positioning. Options markets also reflect comparatively bullish sentiment, with traders maintaining significantly lower downside hedging than Bitcoin.

Gold (XAU): Safe-Haven Demand Accelerates

Gold has benefited directly from weaker employment data and falling expectations for tighter monetary policy.

The precious metal has recovered toward 4,150 USD after several weeks of weakness as declining Treasury yields and a softer U.S. Dollar improved investor appetite for non-yielding assets.

Institutional demand has strengthened as markets increasingly anticipate a more accommodative Federal Reserve policy over coming months.

Market-Wide Recovery Metrics

The entire cryptocurrency market has experienced improving liquidity following the NFP release.

Several important indicators now highlight strengthening market conditions:

• Total crypto market capitalization has expanded alongside Bitcoin's recovery.

• Fear & Greed Index has improved from deeply oversold readings, although sentiment remains within Extreme Fear territory.

• More than 281 million USD in short liquidations accelerated upward momentum as bearish traders were forced to close positions.

• Recent options expiries totaling more than 10 billion USD have contributed to increased market volatility while simultaneously reducing uncertainty heading into the next trading cycle.

Liquidity & Market Structure

Market liquidity has improved noticeably compared with recent weeks.

Stablecoin dominance has started declining, indicating that capital is gradually rotating from defensive positions into higher-risk digital assets.

Long-term holders continue accumulating while short-term supply decreases, suggesting experienced investors are positioning for potential upside over the coming quarters despite cautious institutional ETF flows.

Technical Outlook

Bitcoin

Immediate Resistance • 63,400 USD • 65,000 USD

Major Resistance • 71,000–72,000 USD

Key Support • 60,000 USD

Major Accumulation Zone • 58,000–55,000 USD

A sustained breakout above 64,000–65,000 USD would invalidate the current bearish technical structure and significantly improve the probability of a broader market recovery.

Risk Assessment

Despite improving sentiment, several risks remain.

Institutional ETF flows continue to reflect net selling over longer timeframes.

Mining economics remain under pressure, with production costs still above prevailing market prices, forcing many miners to liquidate reserves.

Historical market cycles also suggest that July frequently delivers relief rallies during bear markets, while August has often produced renewed volatility and downside pressure.

These factors indicate that investors should remain disciplined rather than assuming the current recovery automatically marks the beginning of a new bull market.

Trading Strategy

Bitcoin (BTC)

Accumulation Zone: 60,000–58,000 USD

Breakout Confirmation: Above 65,000 USD

Bullish Target: 71,000–72,000 USD

Extended Target: 75,000–78,000 USD

Solana (SOL)

Strong momentum leader with the highest upside potential during risk-on conditions.

Sustained strength could open a move toward significantly higher price levels if institutional inflows accelerate.

XRP

Suitable for investors seeking comparatively lower volatility with improving institutional participation.

Continued regulatory clarity may support gradual long-term appreciation.

Market Outlook

The weaker NFP report has improved macroeconomic conditions for risk assets and created a favorable short-term environment for cryptocurrencies. Liquidity has strengthened, the U.S. dollar has weakened, and market sentiment has begun recovering from extremely depressed levels.

However, sustainable upside will ultimately depend on continued institutional capital inflows rather than short-covering alone. If Bitcoin successfully establishes support above 60,000 USD and breaks 65,000 USD, the broader cryptocurrency market could enter a much stronger recovery phase led by Bitcoin, Solana, and XRP.

Until then, disciplined accumulation, proper risk management, and close monitoring of macroeconomic developments remain the most prudent strategy for investors.

@Gate_Square

The cryptocurrency market has staged a meaningful recovery after the weaker-than-expected June Non-Farm Payrolls (NFP) report reduced expectations for another Federal Reserve rate hike. The softer labor data weakened the U.S. dollar, improved overall market liquidity, and boosted demand for both digital assets and traditional safe havens such as gold.

Although the recovery has been impressive, investors should recognize that the rally has been driven by a combination of improving macroeconomic sentiment, aggressive short covering, and renewed speculative activity rather than broad institutional accumulation.

This distinction will determine whether the current move evolves into a sustainable uptrend or remains a temporary relief rally.

Bitcoin (BTC): Institutional Recovery with Cautious Optimism

Bitcoin has recovered from approximately 57,000 USD to around 62,850 USD, representing a gain of more than 10 percent from recent lows. Weekly performance has improved to roughly 5.15 percent, while daily gains continue to hold near 1 percent, confirming renewed buying momentum.

Trading activity remains exceptionally healthy.

The BTC/USDT pair on Gate has recorded hundreds of millions of dollars in daily trading volume, demonstrating that this recovery is supported by genuine market participation rather than thin liquidity.

Bitcoin's market capitalization has recovered to nearly 1.24 trillion USD, while U.S. Spot Bitcoin ETFs ended a prolonged outflow streak with approximately 224 million USD of fresh inflows.

Nevertheless, cumulative institutional flows over the previous month remain deeply negative at approximately 6.27 billion USD, suggesting that large investors continue to approach the market cautiously.

Derivative markets remain balanced with neutral funding rates and steadily rising open interest.

Options positioning, however, continues to favor downside protection, indicating that professional traders are maintaining defensive hedges despite recent price appreciation.

Solana (SOL): The Strongest Large-Cap Performer

Solana has emerged as the strongest performer among major cryptocurrencies.

SOL has gained nearly 18.6 percent during the past week, significantly outperforming Bitcoin and most leading digital assets. The network now carries a market capitalization approaching 47 billion USD while maintaining one of the highest growth rates among Layer-1 ecosystems.

One of the primary catalysts behind Solana's strength has been the explosive expansion of tokenized equity trading. Daily trading activity surrounding tokenized stocks has increased dramatically, generating billions of dollars in network volume and attracting fresh liquidity into the ecosystem.

Perpetual futures trading also reflects elevated investor participation, with Solana recording substantially higher derivatives volume than many competing large-cap cryptocurrencies.

This combination of growing ecosystem activity, institutional attention, and increasing liquidity continues to position Solana as one of the highest-beta assets during improving market conditions.

XRP: Stable Institutional Demand Continues

XRP has also participated strongly in the broader recovery.

The asset has appreciated approximately 10 percent over the week while maintaining healthy daily trading volume above 1.5 billion USD.

XRP's market capitalization remains near 70 billion USD, supported by growing institutional adoption and improving regulatory clarity.

Unlike Solana, XRP's performance is driven less by speculative momentum and more by payment infrastructure adoption and long-term institutional positioning. Options markets also reflect comparatively bullish sentiment, with traders maintaining significantly lower downside hedging than Bitcoin.

Gold (XAU): Safe-Haven Demand Accelerates

Gold has benefited directly from weaker employment data and falling expectations for tighter monetary policy.

The precious metal has recovered toward 4,150 USD after several weeks of weakness as declining Treasury yields and a softer U.S. Dollar improved investor appetite for non-yielding assets.

Institutional demand has strengthened as markets increasingly anticipate a more accommodative Federal Reserve policy over coming months.

Market-Wide Recovery Metrics

The entire cryptocurrency market has experienced improving liquidity following the NFP release.

Several important indicators now highlight strengthening market conditions:

• Total crypto market capitalization has expanded alongside Bitcoin's recovery.

• Fear & Greed Index has improved from deeply oversold readings, although sentiment remains within Extreme Fear territory.

• More than 281 million USD in short liquidations accelerated upward momentum as bearish traders were forced to close positions.

• Recent options expiries totaling more than 10 billion USD have contributed to increased market volatility while simultaneously reducing uncertainty heading into the next trading cycle.

Liquidity & Market Structure

Market liquidity has improved noticeably compared with recent weeks.

Stablecoin dominance has started declining, indicating that capital is gradually rotating from defensive positions into higher-risk digital assets.

Long-term holders continue accumulating while short-term supply decreases, suggesting experienced investors are positioning for potential upside over the coming quarters despite cautious institutional ETF flows.

Technical Outlook

Bitcoin

Immediate Resistance • 63,400 USD • 65,000 USD

Major Resistance • 71,000–72,000 USD

Key Support • 60,000 USD

Major Accumulation Zone • 58,000–55,000 USD

A sustained breakout above 64,000–65,000 USD would invalidate the current bearish technical structure and significantly improve the probability of a broader market recovery.

Risk Assessment

Despite improving sentiment, several risks remain.

Institutional ETF flows continue to reflect net selling over longer timeframes.

Mining economics remain under pressure, with production costs still above prevailing market prices, forcing many miners to liquidate reserves.

Historical market cycles also suggest that July frequently delivers relief rallies during bear markets, while August has often produced renewed volatility and downside pressure.

These factors indicate that investors should remain disciplined rather than assuming the current recovery automatically marks the beginning of a new bull market.

Trading Strategy

Bitcoin (BTC)

Accumulation Zone: 60,000–58,000 USD

Breakout Confirmation: Above 65,000 USD

Bullish Target: 71,000–72,000 USD

Extended Target: 75,000–78,000 USD

Solana (SOL)

Strong momentum leader with the highest upside potential during risk-on conditions.

Sustained strength could open a move toward significantly higher price levels if institutional inflows accelerate.

XRP

Suitable for investors seeking comparatively lower volatility with improving institutional participation.

Continued regulatory clarity may support gradual long-term appreciation.

Market Outlook

The weaker NFP report has improved macroeconomic conditions for risk assets and created a favorable short-term environment for cryptocurrencies. Liquidity has strengthened, the U.S. dollar has weakened, and market sentiment has begun recovering from extremely depressed levels.

However, sustainable upside will ultimately depend on continued institutional capital inflows rather than short-covering alone. If Bitcoin successfully establishes support above 60,000 USD and breaks 65,000 USD, the broader cryptocurrency market could enter a much stronger recovery phase led by Bitcoin, Solana, and XRP.

Until then, disciplined accumulation, proper risk management, and close monitoring of macroeconomic developments remain the most prudent strategy for investors.

@Gate_Square