Perpetual Futures have become one of the most critical trading products in the DeFi derivatives market. As on-chain trading demand grows, multiple protocols are exploring different liquidity architectures and risk management models to address issues like insufficient liquidity, high slippage, and limited capital efficiency in traditional decentralized exchanges.

CyberDEX and GMX represent two distinctive approaches in this space. Both offer on-chain Perpetual Futures trading and seek to reduce reliance on market makers inherent in traditional order book models. However, they differ significantly in liquidity sources, risk allocation, and protocol design philosophy.

What Is CyberDEX?

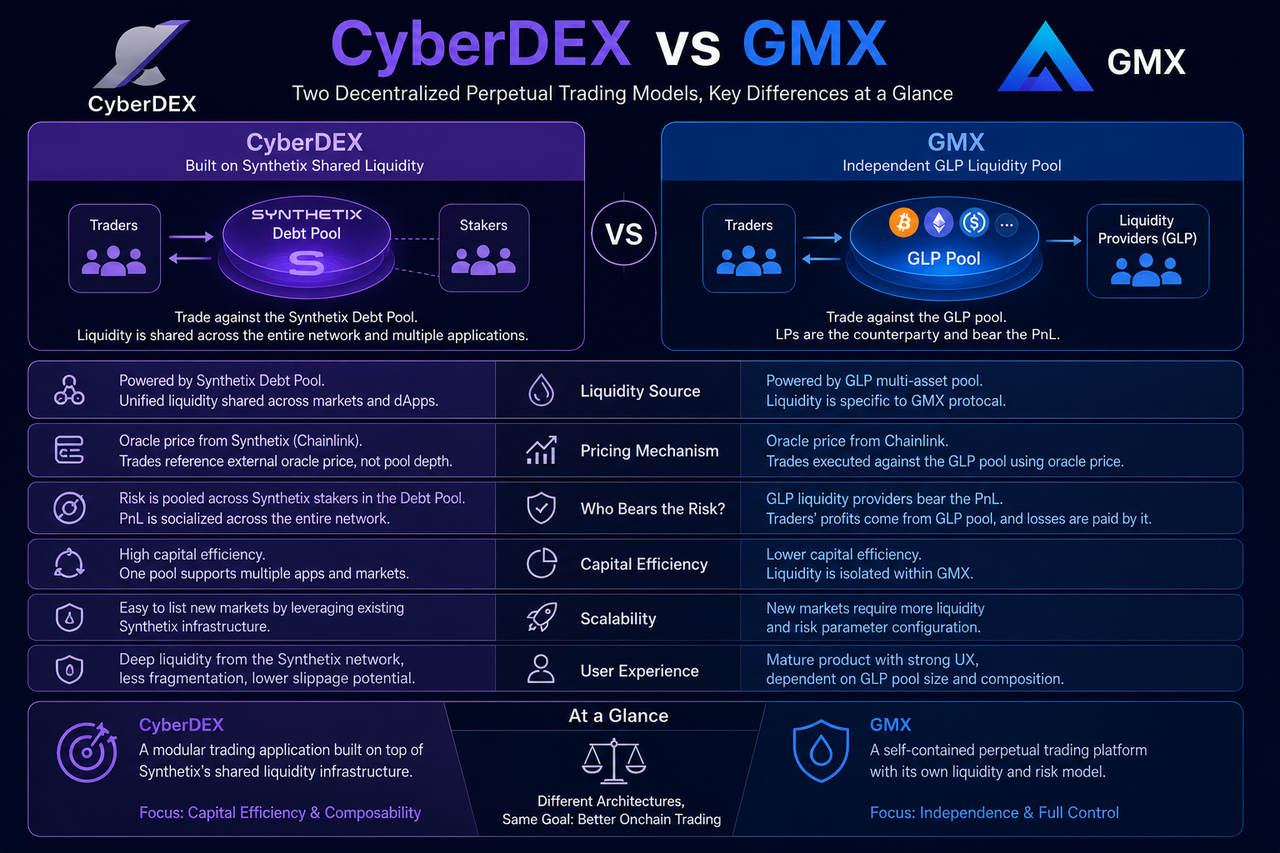

CyberDEX is a decentralized Perpetual Futures trading platform built on the Optimism network, distinguished by its integration with the shared liquidity network provided by Synthetix. When users trade on CyberDEX, they essentially interact with Synthetix's Debt Pool, rather than relying on independent liquidity pools or traditional market makers to execute orders.

This approach allows CyberDEX to leverage existing liquidity infrastructure for rapid market expansion while avoiding redundant construction of underlying capital pools. The platform focuses primarily on trading product design, user experience optimization, and derivatives innovation, while liquidity management remains under Synthetix's purview.

Consequently, CyberDEX functions more as an application-layer protocol built on a shared financial infrastructure.

What Is GMX?

GMX is one of the most prominent Perpetual Futures trading platforms in the Arbitrum and Avalanche ecosystems. Unlike CyberDEX, GMX does not depend on an external liquidity network; instead, it operates its own GLP liquidity pool system.

GLP is a multi-crypto asset liquidity pool where liquidity providers deposit assets to earn Rendite. When traders open positions, they effectively trade against the GLP pool, making GLP providers the direct counterparty to traders.

This model gives GMX full control over its liquidity system but also requires independent maintenance of market liquidity and risk balance.

What Is the Difference in Liquidity Sources?

Liquidity source is one of the most significant distinctions between CyberDEX and GMX.

CyberDEX draws its liquidity from the Synthetix Debt Pool. All assets participating in the Synthetix staking system form a unified debt pool that supports multiple applications. Thus, CyberDEX does not maintain its own liquidity pool; instead, it shares the Markttiefe of the entire Synthetix network.

GMX, by contrast, adopts the GLP multi-asset pool model. Liquidity is created by users actively depositing assets, and trading depth depends on the size and asset composition of the GLP pool.

| Comparison Dimension |

CyberDEX |

GMX |

| Liquidity Source |

Synthetix Debt Pool |

GLP Multi-Asset Pool |

| Shared Liquidity |

Yes |

No |

| Liquidity Ownership |

Synthetix Network |

GMX Protocol |

| Cost of Expanding to New Markets |

Lower |

Relatively Higher |

| Capital Efficiency |

Higher |

Medium |

Shared liquidity reduces fragmentation, while independent liquidity offers stronger autonomous control.

How Do the Pricing Mechanisms Differ?

Though both CyberDEX and GMX employ oracle-based pricing, their implementations differ.

CyberDEX's pricing is grounded in Synthetix's Synthetik framework. Oracle prices serve directly as the trading reference, with no reliance on order book depth.

GMX also uses oracle prices to execute trades. However, because traders face the GLP pool, their activity directly influences the pool's overall risk exposure.

This divergence implies different logic in risk distribution and market balancing mechanisms.

Who Bears the Trading Risk?

Risk allocation is key to understanding the differences between the two models.

In CyberDEX, risk is ultimately shared by all Synthetix Debt Pool participants. Since all staked assets form a unified debt pool, market gains and losses are distributed across the entire system.

In GMX, GLP liquidity providers directly absorb traders' gains and losses. When traders are collectively profitable, the GLP pool's asset value may decline; when traders collectively lose, GLP providers may benefit.

Thus, each model presents a distinct risk structure.

| Risk Bearing Entity |

CyberDEX |

GMX |

| Primary Risk Bearer |

Debt Pool Participants |

GLP Holders |

| Degree of Risk Diversification |

Higher |

Relatively Concentrated |

| Role of Liquidity Providers |

System Participant |

Counterparty to Trades |

| Profit/Loss Distribution Method |

Shared Across the Network |

Borne Within the GLP Pool |

This difference impacts the Rendite sources and risk profiles of liquidity providers.

Which Has Better Capital Efficiency and Scalability?

Capital efficiency is a key metric in DeFi protocol design.

CyberDEX, by sharing Synthetix's unified liquidity pool, allows the same capital to serve multiple applications and markets simultaneously. This reduces duplicate liquidity requirements and enhances overall capital utilization.

GMX's liquidity serves only its own protocol, so expanding to new trading markets typically demands more liquidity support. While this model offers greater independence, its capital utilization efficiency is comparatively lower.

Given the trend toward modular finance, the shared liquidity model aligns better with the separation of infrastructure and application layers.

What Are the Differences in User Trading Experience?

For ordinary traders, both platforms deliver a Perpetual Futures trading experience akin to centralized exchanges.

CyberDEX's advantage lies in accessing unified Markttiefe from the Synthetix network and mitigating the effects of market fragmentation. As shared liquidity scales, the trading experience improves accordingly.

GMX, with its mature product suite and independent liquidity architecture, has built a strong user base. Its trading experience depends heavily on the size and asset structure of the GLP liquidity pool.

Functionally, both support leveraged trading, long/Short-Position, and self-custody of on-chain assets. Therefore, the core differences remain rooted in the underlying liquidity architecture.

Summary of Core Differences Between CyberDEX and GMX

On the surface, both CyberDEX and GMX are decentralized Perpetual Futures trading platforms, but they represent two distinct development paths.

CyberDEX builds its trading application by leveraging Synthetix's shared liquidity network, prioritizing capital efficiency and reduced liquidity fragmentation. GMX, in contrast, establishes a fully independent liquidity system, achieving protocol autonomy through the GLP pool.

| Core Dimension |

CyberDEX |

GMX |

| Basic Architecture |

Synthetix Ecosystem Application Layer |

Independent Protocol System |

| Liquidity Model |

Debt Pool |

GLP Pool |

| Capital Efficiency |

Higher |

Medium |

| Protocol Autonomy |

Lower |

Higher |

| Risk Bearer |

Debt Pool |

GLP Holders |

| Development Path |

Modular Shared Liquidity |

Independent Liquidity System |

Neither model is inherently superior; they simply make different trade-offs in capital efficiency, autonomy, and risk structure.

Conclusion

CyberDEX and GMX are both major players in the DeFi Perpetual Futures market, but their underlying design philosophies differ fundamentally.

CyberDEX achieves Markttiefe by tapping into Synthetix's shared liquidity network, reflecting the modular finance trajectory. GMX, relying on its self-built GLP liquidity pool for independent operation, represents the path of early DeFi derivatives protocols. As DeFi infrastructure matures, both shared and independent liquidity models are likely to coexist long term.

FAQs

Yes. Both CyberDEX and GMX provide on-chain Perpetual Futures trading, supporting long/Short-Position and leveraged trading, though their underlying liquidity architectures differ.

Why does CyberDEX rely on Synthetix?

CyberDEX leverages Synthetix's shared liquidity network and Synthetik infrastructure to avoid building its own liquidity pool, thereby improving capital efficiency.

What is GMX's GLP?

GLP is GMX's multi-asset liquidity pool, composed of various crypto assets. GLP holders provide market liquidity and bear the risk corresponding to traders' gains and losses.

Is CyberDEX's liquidity larger than GMX's?

The two differ in liquidity sources. CyberDEX can access the entire Synthetix network's liquidity, while GMX depends on its own GLP pool size. Therefore, liquidity depth depends on each ecosystem's development.

Which model offers higher capital efficiency?

From a design perspective, the shared liquidity model typically reduces redundant liquidity construction, making it relatively more capital efficient. However, actual performance depends on protocol scale and market participation.