In the decentralized derivatives space, liquidity has always been a critical factor influencing trading experience and market efficiency. The introduction of GM Pool allows GMX to support large-scale leveraged trading without an order book or market maker system, making it a vital component of GMX's ecosystem operations and risk management.

What Is GM Pool?

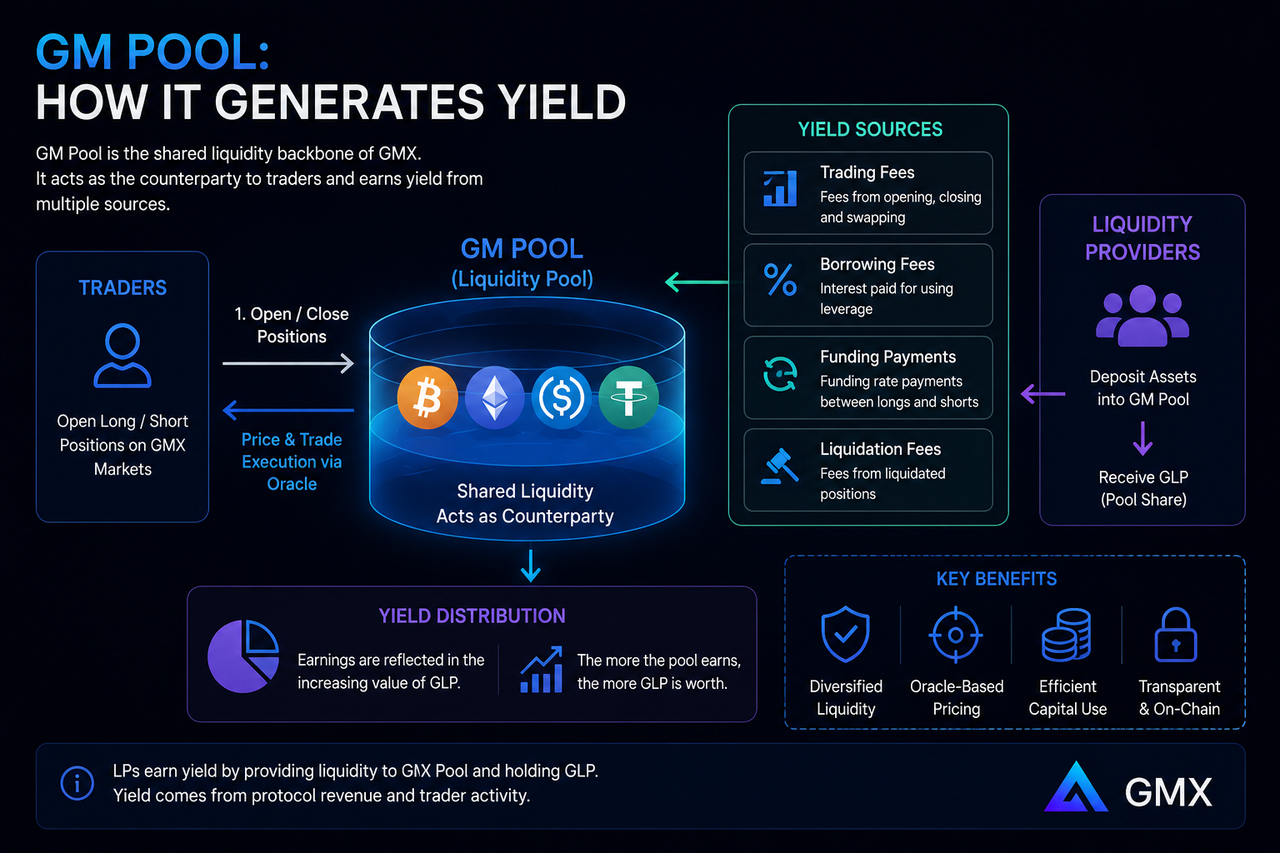

GM Pool serves as the core liquidity pool for GMX V2, providing capital support for specific trading markets. Each GM Pool is typically built around a single trading market and holds a corresponding portfolio of assets.

When traders open long or short positions on GMX, the GM Pool acts as the unified counterparty. All trader profits and losses are ultimately reflected in changes to the liquidity pool's asset value.

Thus, GM Pool not only provides liquidity but also absorbs market risk.

How Is GM Pool Different from Traditional AMM Liquidity Pools?

While GM Pool and AMM liquidity pools like Uniswap both use a fund pool structure, their underlying logic is fundamentally different.

Traditional AMMs primarily facilitate token swaps and determine prices based on the asset ratio within the pool. GM Pool, by contrast, relies on oracle prices for trade execution and is designed primarily for the perpetual futures market.

The key difference lies in risk exposure. AMMs face impermanent loss risk, while GM Pool is more concerned with the risk arising from traders' overall profit and loss.

| Dimension |

GM Pool |

Traditional AMM |

| Primary Use |

Perpetual futures liquidity |

Spot swaps |

| Pricing Source |

Oracle prices |

Pool asset ratio |

| Counterparty Role |

Liquidity pool acts as counterparty |

Swaps between users |

| Revenue Source |

Trading fees and activity |

Transaction fees |

| Core Risk |

Trader profitability risk |

Impermanent loss |

How Does GM Pool Generate Revenue?

GM Pool's revenue comes from multiple streams, consisting of various fees generated during protocol operation.

When liquidity providers deposit assets into GM Pool, they receive corresponding pool shares. As protocol income grows, the pool's asset value increases, and the value of each share rises accordingly.

This design makes GM Pool a key link between trading activity and liquidity provider returns.

Trading Fee Revenue

Trading fees are one of GM Pool's most stable income sources.

Every time a user performs a spot trade, opens or closes a position, or adjusts their position, they pay a fee. A portion of these fees flows into the liquidity pool and is distributed to liquidity providers based on their share of the pool.

The more active the market, the higher the trading fee revenue tends to be.

Borrowing Fee Revenue

Perpetual futures trading requires capital from the liquidity pool, so traders pay borrowing fees.

Borrowing fees are dynamically adjusted based on market capital utilization. When leverage demand rises, borrowing fees typically increase, boosting potential returns for liquidity providers.

Dynamic Funding Fees

To maintain market balance, GMX uses a dynamic fee mechanism to regulate position sizes across different directions.

A portion of these fees enters the liquidity pool, forming a significant part of GM Pool's revenue.

This mechanism encourages a healthier capital structure in the market.

Why Do Trader Losses Affect GM Pool Revenue?

GM Pool is essentially the unified counterparty for all traders.

When traders overall are profitable, the profits must be paid out of the liquidity pool, reducing its asset size. When traders overall are losing, the corresponding funds flow into the liquidity pool, increasing its asset value.

This means GM Pool's revenue is directly tied to traders' collective performance.

In the long run, protocol income typically comes from fees and market trading activity, not solely from trader losses.

How Is GM Pool Revenue Distributed?

Revenue distribution is calculated based on the pool shares held by liquidity providers.

When users supply assets to the liquidity pool, the system calculates shares based on the deposited asset value. As pool assets grow, the value per share increases.

Liquidity providers don't need to actively trade; returns are reflected directly in the changing value of their shares.

What Risks Does GM Pool Face?

While GM Pool can earn protocol income, it also bears certain market risks.

The biggest risk comes from overall trader profitability. During a sustained one-sided market trend, many successful traders may withdraw profits from the pool, reducing its assets.

Liquidity providers should also be aware of the following risks:

Market Volatility Risk

Extreme market conditions can cause a large number of positions to become profitable or unprofitable in a short time, affecting pool asset value.

Oracle Risk

GMX's price system relies on an oracle network. Abnormal price data could disrupt normal market operations.

Liquidity Risk

In extreme market environments, the liquidity pool may face higher capital utilization and expanded risk exposure.

Summary

As the core liquidity infrastructure of GMX V2, GM Pool supports both spot and perpetual futures markets by acting as a unified counterparty. Unlike traditional AMM pools, GM Pool uses oracle prices and takes on market risk management.

GM Pool's revenue primarily comes from trading fees, borrowing fees, dynamic fees, and the capital flow generated by market activity. At the same time, liquidity providers must manage trader profitability risk and market volatility.

FAQs

What Is GM Pool?

GM Pool is the liquidity pool system for GMX V2, providing liquidity for spot and perpetual futures markets and acting as a unified counterparty for traders.

Where Does GM Pool's Revenue Come From?

GM Pool's revenue comes mainly from trading fees, borrowing fees, dynamic fees, and capital flow from trading activity.

How Is GM Pool Different from Traditional AMM?

GM Pool uses oracle prices for trading and serves the derivatives market; traditional AMMs rely on pool asset ratios for pricing and are used for spot swaps.

Why Do Trader Losses Increase GM Pool Revenue?

Because GM Pool is the counterparty. When traders lose, the funds flow into the liquidity pool, increasing its asset value.

Is GM Pool Risky?

GM Pool carries market volatility risk, trader profitability risk, oracle risk, and liquidity risk, so returns are not fixed.

Who Can Become a GM Pool Liquidity Provider?

Any user meeting the protocol's requirements can provide assets to GM Pool and share in the revenue generated during protocol operation based on their holdings.