#PYTHUnlocks2.13BillionTokens The Narrative Shift: COVID to Catalyst Platform

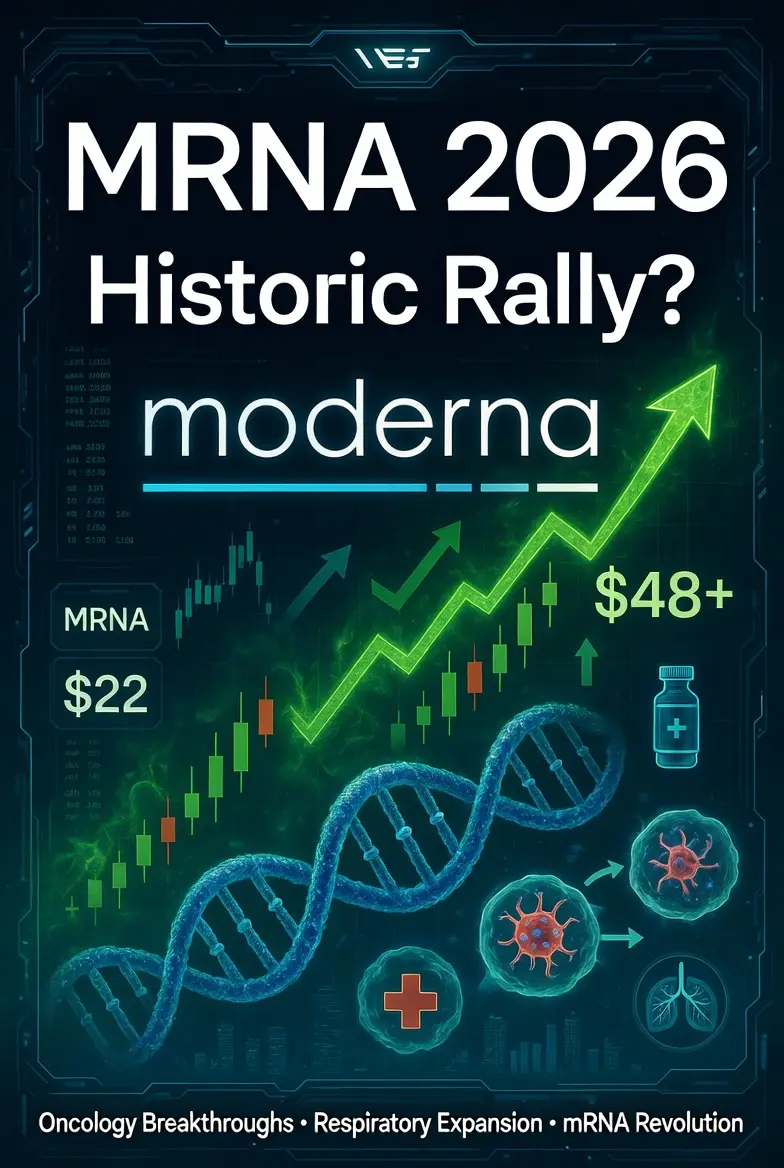

Moderna's massive valuation collapse from its $497 peak occurred because the market priced it strictly as a COVID-19 vaccine manufacturer. The current 2026 rally signals that Wall Street is beginning to value its core mRNA infrastructure. Instead of looking at individual products, institutional investors are evaluating the company's ability to quickly program genetic code for a massive array of indications.

🚀 Key Growth Pillars & 2026 Catalysts

The Respiratory Franchise: While COVID revenues have dried up, the successful Phase 3 performance of mRNA-1010 (Flu) and the rollout of mRESVIA (RSV) mean Moderna can establish stable, seasonal commercial revenues.

The Hantavirus Sentiment Spike: The recent cruise-ship-related hantavirus headline sparked an aggressive 20% short-term rally (pushing the stock briefly past $54). While smart money views this purely as a sentiment catalyst rather than immediate revenue, it vividly proved to the market that Moderna can pivot to new infectious disease threats faster than traditional pharma.

The Merck Oncology Mega-Catalyst: The ultimate "make-or-break" factor remains Intismeran (mRNA-4157). Personalized cancer vaccines represent a multi-billion-dollar paradigm shift. If late-stage melanoma or non-small-cell lung cancer (NSCLC) data misses the mark, the valuation will contract swiftly; if it succeeds, $48 will look like a distant memory.

Technical & Financial Breakdown

Moderna is currently locked in a classic battle between an improved scientific outlook and tough financial realities.Market Outlook: The Verdict

The high short interest (~16%) tells us that a large segment of Wall Street remains highly skeptical of Moderna's path to profitability, pointing out that its 2026 EPS is still deeply negative. However, with $7.5 billion in cash, Moderna has a long enough runway to see its Phase 3 oncology and combination respiratory pipelines mature.

The technical "line in the sand" sits around the mid-$40s. As long as macro biotech sentiment remains healthy and the stock holds above this structural support zone, the broader trend points to an accumulation phase rather than a speculative bubble.

Moderna's massive valuation collapse from its $497 peak occurred because the market priced it strictly as a COVID-19 vaccine manufacturer. The current 2026 rally signals that Wall Street is beginning to value its core mRNA infrastructure. Instead of looking at individual products, institutional investors are evaluating the company's ability to quickly program genetic code for a massive array of indications.

🚀 Key Growth Pillars & 2026 Catalysts

The Respiratory Franchise: While COVID revenues have dried up, the successful Phase 3 performance of mRNA-1010 (Flu) and the rollout of mRESVIA (RSV) mean Moderna can establish stable, seasonal commercial revenues.

The Hantavirus Sentiment Spike: The recent cruise-ship-related hantavirus headline sparked an aggressive 20% short-term rally (pushing the stock briefly past $54). While smart money views this purely as a sentiment catalyst rather than immediate revenue, it vividly proved to the market that Moderna can pivot to new infectious disease threats faster than traditional pharma.

The Merck Oncology Mega-Catalyst: The ultimate "make-or-break" factor remains Intismeran (mRNA-4157). Personalized cancer vaccines represent a multi-billion-dollar paradigm shift. If late-stage melanoma or non-small-cell lung cancer (NSCLC) data misses the mark, the valuation will contract swiftly; if it succeeds, $48 will look like a distant memory.

Technical & Financial Breakdown

Moderna is currently locked in a classic battle between an improved scientific outlook and tough financial realities.Market Outlook: The Verdict

The high short interest (~16%) tells us that a large segment of Wall Street remains highly skeptical of Moderna's path to profitability, pointing out that its 2026 EPS is still deeply negative. However, with $7.5 billion in cash, Moderna has a long enough runway to see its Phase 3 oncology and combination respiratory pipelines mature.

The technical "line in the sand" sits around the mid-$40s. As long as macro biotech sentiment remains healthy and the stock holds above this structural support zone, the broader trend points to an accumulation phase rather than a speculative bubble.