Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Pre-IPOs

Unlock full access to global stock IPOs

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

Goldman Sachs applies for Bitcoin yield ETF: How covered call strategies turn volatility into monthly cash flow

On April 14, 2026, Goldman Sachs, a top global investment bank with over 150 years of history, submitted a document to the U.S. Securities and Exchange Commission that has drawn significant market attention—applying to launch its first proprietary Bitcoin fund product, the “Goldman Sachs Bitcoin Premium Yield ETF.” Unlike existing spot Bitcoin ETFs in the market, this product does not hold Bitcoin directly but gains income by holding shares of spot Bitcoin exchange-traded products and systematically selling call options to collect premiums, converting Bitcoin’s volatility into regular income. This strategic shift reflects a deep evolution in how Wall Street’s major financial institutions view crypto assets: from questioning “whether to allocate Bitcoin” to “how to allocate Bitcoin more efficiently.”

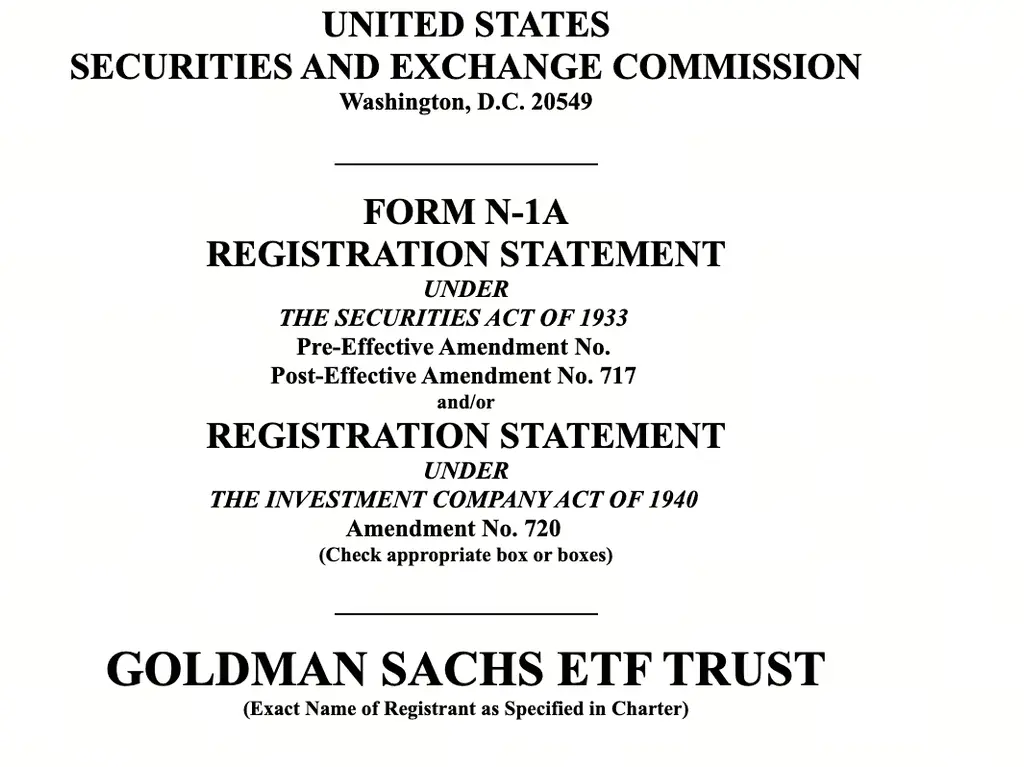

Goldman Sachs’ First Proprietary Bitcoin ETF Proposal Emerges

On April 14, 2026, Goldman Sachs Asset Management filed an initial prospectus with the SEC for the “Goldman Sachs Bitcoin Premium Yield ETF.” According to the filing, the fund plans to invest at least 80% of its net assets in instruments that provide Bitcoin exposure, mainly including shares of existing spot Bitcoin ETFs, Bitcoin ETF options, and Bitcoin ETF index options.

Source: Document submitted by Goldman Sachs

The core strategy of this product is covered call writing. While holding long positions in spot Bitcoin ETFs, the fund systematically sells corresponding call options, collecting premiums from option buyers, and distributes this income as periodic returns to investors. The filing discloses that under normal market conditions, the option coverage ratio will be maintained between 40% and 100% of Bitcoin exposure, with the specific ratio dynamically adjusted based on market conditions.

Notably, Goldman Sachs has not disclosed the proposed management fee rate in this filing. Following standard regulatory review procedures, the product is expected to be listed and traded approximately 75 days after filing, earliest around late June to early July 2026. The trading symbol and specific listing exchange have not yet been determined.

Wall Street Giants’ Crypto Turnaround: From Skepticism to Proprietary Products Over Nine Years

Goldman Sachs’ ETF application is not an isolated event but a latest chapter in a nearly decade-long narrative evolution.

In September 2017, JPMorgan Chase CEO publicly called Bitcoin a “scam” and warned that employees trading Bitcoin would be fired. At that time, mainstream Wall Street financial institutions generally distanced themselves from or explicitly rejected crypto assets.

In 2021, Goldman Sachs revived its crypto trading desk, beginning to offer Bitcoin futures and options services to clients, but maintained a relatively cautious stance.

Between 2024 and 2025, Goldman Sachs’ 13F filings gradually revealed its true asset allocation. By Q4 2024, Goldman held about $1.57 billion in Bitcoin ETF shares, with BlackRock’s IBIT accounting for the largest portion at approximately $1.27 billion. By Q4 2025, Goldman’s indirect Bitcoin holdings equated to roughly 13,741 BTC, along with about $1 billion in Ethereum ETFs, $153 million in XRP ETFs, and $108 million in Solana ETFs.

On April 8, 2026, Goldman’s main competitor, Morgan Stanley, launched its own spot Bitcoin ETF, with a fee rate of just 0.14%, setting a record low for similar products, attracting about $34 million in inflows on the first day.

On April 14, 2026, Goldman Sachs officially submitted an application for its first proprietary Bitcoin ETF, marking a transition from “buying others’ products” to “issuing its own products.”

Covered Call Strategy Analysis: Differentiating Spot ETFs and Income-Generating Products

From a product structure perspective, Goldman Sachs’ Bitcoin Premium Yield ETF fundamentally differs from existing mainstream Bitcoin investment products.

Below is a comparison of four representative Bitcoin investment products:

The core innovation of Goldman’s product lies in its income generation mechanism. In traditional spot ETFs, investor returns depend entirely on Bitcoin’s price movements. In Goldman’s structure, the fund continuously sells call options to collect premiums, which can be distributed as income regardless of Bitcoin’s price trend.

According to the filing, the option coverage ratio will be dynamically adjusted between 40% and 100%. This range grants fund managers significant flexibility: in periods of expected stable or mildly rising markets, they can increase coverage to maximize premium income; in scenarios anticipating sharp upward moves, they can reduce coverage to retain more upside participation.

Another noteworthy aspect is that Goldman has not disclosed the management fee rate in this application. Under normal review processes, the product is expected to be approved and listed around late June to early July 2026. The trading symbol and exchange are yet to be determined.

This ETF application also has an important background: earlier in 2026, Goldman acquired Innovator Capital Management for about $2 billion. Innovator is a pioneer in buffer ETFs, having launched the first U.S. buffer ETF in 2018, specializing in using options strategies to build income-oriented products. This acquisition provides Goldman with mature options management capabilities and product design experience, facilitating rapid development of a Bitcoin income-focused ETF.

Market Opinions Diverge: Institutional Demand Signals and Strategy Effectiveness Debate

Market commentary on Goldman’s application shows clear divergence, with different analytical perspectives offering varied interpretations.

Bloomberg ETF analyst Eric Balchunas commented on social media that Goldman’s move might be a response to client demand for low-volatility Bitcoin exposure. He wrote: “Goldman may see an opportunity to surpass competitors, or more likely, they’ve heard their clients—who want Bitcoin but with less volatility—and are willing to trade some upside potential for lower drawdowns and regular income.” He also vividly described the product as a “baby boomer’s candy,” implying it precisely targets traditional investors seeking stable cash flow.

Morningstar ETF analyst Bryan Armour expressed a more cautious view. He noted: “Adding options income to the product is good, but considering Bitcoin’s inherent volatility and the fact that the product still exposes investors to downside risk, it might be a hard sell.”

Industry insiders have pointed out that Goldman’s covered call strategy essentially replicates a mature income-enhancement model from traditional finance—simply monetizing Bitcoin’s volatility. Summit Gupta commented on Morgan Stanley’s MSBT, saying: “Seeing a global giant like Morgan Stanley prominently feature crypto on their website is a very positive signal. Traditional finance is no longer just a bystander; it’s actively prioritizing and scaling crypto assets as a core asset class.”

Overall, positive market feedback on Goldman’s product mainly focuses on three aspects: first, providing institutional investors with a familiar income framework; second, broadening Bitcoin asset allocation scenarios; third, marking a shift from “investment” to “product creation” by traditional financial giants in crypto. Negative concerns center on the inherent limitations of covered call strategies in bull markets and the high volatility of Bitcoin potentially eroding the effectiveness of income strategies.

Industry Landscape Reshaping: From Single Exposure to Multi-Tiered Income Solutions

Goldman Sachs’ application for a Bitcoin Premium Yield ETF can be viewed through several dimensions:

Product matrix evolving from “single exposure” to “multi-layered solutions.” Spot Bitcoin ETFs address the fundamental question of “whether to allocate Bitcoin legally,” while income ETFs tackle the more advanced issue of “how to generate ongoing cash flow while holding Bitcoin.” BlackRock’s BITA, Grayscale’s BPI with about 24.82% annualized distribution, and others indicate that income-oriented crypto ETFs are becoming a clear next-stage track.

Investor composition may become more institutionalized. The design logic of covered call strategies naturally appeals to asset managers with explicit cash flow requirements: these investors often find pure price appreciation insufficient for risk control, whereas regular dividends provide a more traditional and easily integrated narrative.

Market competition is becoming functionally differentiated. Morgan Stanley’s entry with a 0.14% fee in the spot market and Goldman’s focus on income strategies target different risk profiles, avoiding direct homogeneity. Spot ETFs solve “price exposure,” while income ETFs address “cash flow,” and their coexistence will promote a more mature, multi-layered crypto ETF market.

The integration of traditional finance and crypto markets deepens. Goldman’s path—from holding third-party ETFs to issuing proprietary ETFs, from spot exposure to layered derivatives—demonstrates a full recognition upgrade of crypto assets by traditional finance: from “observation” to “investment,” and now to “product manufacturing.” This shift indicates that crypto assets are gradually being incorporated into the core framework of mainstream global asset management.

Multiple Future Scenarios and Evolution Paths

Based on current information, the following market evolution scenarios for Goldman’s Bitcoin income ETF can be envisioned:

Scenario 1: Successful listing and institutional favor

In this scenario, Goldman’s product is approved and listed around July 2026. Leveraging Goldman’s reputation among global institutional investors, it attracts large inflows from insurance funds, pension funds, family offices seeking stable cash flow. The total assets under management of income-oriented crypto ETFs expand rapidly in the second half of 2026, encouraging more traditional institutions to follow suit. The spot and income ETFs form a complementary ecosystem, increasing crypto’s share in traditional asset allocations.

Scenario 2: Listing but facing fierce competition

Here, Goldman’s product is approved and listed but faces strong competition from BlackRock’s BITA and Grayscale’s BPI. If Goldman’s disclosed management fee is not competitive, fund inflows may fall short. Moreover, recent three-month net outflows from existing income Bitcoin ETFs suggest market acceptance is still in development. The competitive landscape may evolve into a combination of fee and brand battles.

Scenario 3: Regulatory review delays or additional conditions

If the SEC imposes extra scrutiny under the 1940 Act framework or demands further clarity on Cayman subsidiary structures, listing could be delayed to Q3 2026 or later. Regulatory attitudes will be a key variable affecting the product’s launch pace. Given recent applications from multiple Wall Street firms, the SEC may prefer a unified review standard and coordinated approval timeline.

Scenario 4: Market experiences extreme volatility

If Bitcoin’s price swings sharply before or after product launch, it will test the boundaries of the covered call strategy’s effectiveness. During sharp declines, premiums can buffer some losses but cannot fully offset NAV declines; during rapid rallies, the sold call options will cap upside, potentially causing the product’s performance to lag behind pure spot ETFs and eroding investor confidence.

Conclusion

Goldman Sachs’ application for a Bitcoin Premium Yield ETF marks a new phase in Wall Street’s crypto narrative. From nine years of skepticism and observation to proactive issuance and strategic innovation, traditional finance’s attitude toward crypto assets has undergone a fundamental transformation. The introduction of a covered call strategy signifies that Bitcoin is no longer merely a speculative tool for price volatility but can be redefined as a financial asset capable of generating sustained income—this shift has profound implications for the mainstreaming of crypto assets.

Of course, the structural design of income ETFs inherently involves trade-offs between yield and upside potential. Investors need to understand the mechanics of the covered call strategy and align their risk preferences and cash flow needs accordingly. For the entire crypto industry, the fact that top global investment banks are beginning to craft income products for Bitcoin itself signals a noteworthy development: crypto assets are being redefined, not simply adopted.