Futures

Access hundreds of perpetual contracts

CFD

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

CFD

U.S. stock CFD derivatives

US Stocks

Access real US stocks and ETFs

HK Stocks

Trade quality Hong Kong-listed stocks

Korean Stocks

SK Hynix

Real Korean stocks and top assets

Stock Futures

High leverage, 24/7 trading

Tokenized Stocks

Backed by real stock assets

IPO Access

Unlock full access to global stock IPOs

GUSD

Mint GUSD for Treasury RWA yields

Stocks Activities

Trade Popular Stocks and Unlock Generous Airdrops

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

IPO Access

Unlock full access to global stock IPOs

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

Promotions

AI

Gate AI

Your all-in-one conversational AI partner

Gate AI Bot

Use Gate AI directly in your social App

GateClaw

Gate Blue Lobster, ready to go

Gate for AI Agent

AI infrastructure, Gate MCP, Skills, and CLI

Gate Skills Hub

10K+ Skills

From office tasks to trading, the all-in-one skill hub makes AI even more useful.

The upgrade cycle narrative has hit a setback, as a UBS survey shows Apple's AI features have failed to ignite a replacement wave.

Apple Intelligence, Apple's AI feature, has failed to become the catalyst for the iPhone upgrade supercycle that Wall Street expected. UBS's latest survey shows that consumers' willingness to upgrade devices early due to AI features continues to decline, putting renewed pressure on market confidence in Apple's AI-driven growth narrative.

According to the latest report from UBS analyst David Vogt, his Evidence Lab survey of over 7,500 smartphone users across five major markets shows that about 24% of respondents said they would upgrade their phones early due to Apple Intelligence, down about 500 basis points from the first half of the year; at the same time, the proportion of those who think AI features have 'no impact' on purchase decisions rose to about 31%, up about 300 basis points. This result indicates that Apple's core logic of using AI features to drive a new round of hardware upgrade cycles has not yet translated into effective consumer conversion, and it also makes some investors question the sustainability of further valuation expansion. Apple Intelligence's upgrade driving power weakens

UBS pointed out that Apple Intelligence has not yet materially spurred user upgrades, and the market's previously anticipated 'AI-driven upgrade cycle' has not materialized. Although iPhone purchase intentions in the US, UK, and German markets rose by about 300, 600, and 400 basis points year-over-year respectively, showing relative stability, UBS analyst Vogt believes that the AI features Apple released at WWDC26 will still struggle to become a key driver of demand in the short term. Against the backdrop of cooling AI narratives, the foldable iPhone has become one of the few emotional support points. Although the overall foldable phone market's 'net interest' declined by about 600 basis points to -8%, consumers' preference for 'Apple-brand foldable screens' is significantly stronger, with the relative premium expanding by about 600 basis points to around 48%. UBS expects that Apple is likely to launch its first foldable iPhone at its September annual conference, which could bring an initial incremental sales volume of about 5 million units, equivalent to about 2% upside to its iPhone shipment forecast. Shipment growth and valuation constraints coexist; Apple awaits new product validation

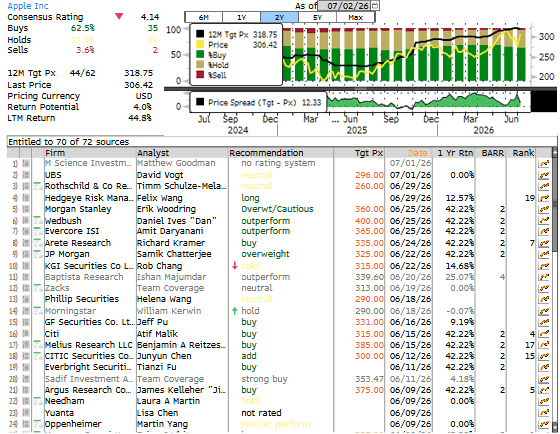

UBS expects Apple's FY26 iPhone shipments to reach approximately 261.6 million units, up about 15.7% year-over-year, mainly driven by stronger demand for the iPhone 17 and potential pre-demand due to price increases. In terms of valuation, UBS maintains its Apple price target of $296, based on FY2027 EPS of $9.86 and a 30x P/E ratio assumption. The firm believes that the current stock price already partially reflects short-term iPhone demand improvement and AI option value, but product roadmap uncertainty, weak China market conditions, and pricing factors limit further upside potential for valuation. According to consensus estimates, Wall Street still maintains a mostly positive stance on Apple overall: 35 analysts give a 'Buy' rating, 19 'Hold', 2 'Sell', with a 12-month average price target of about $319. Apple's stock price has now returned above $300. Against the backdrop of the unfulfilled AI-driven upgrade logic, the market's focus is gradually shifting from 'technology narrative' to 'hardware cycle and product launch cadence'. Risk Warning and Disclaimer

Risk Warning and Disclaimer