Futures

Access hundreds of perpetual contracts

CFD

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Pre-IPOs

Unlock full access to global stock IPOs

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

Promotions

AI

Gate AI

Your all-in-one conversational AI partner

Gate AI Bot

Use Gate AI directly in your social App

GateClaw

Gate Blue Lobster, ready to go

Gate for AI Agent

AI infrastructure, Gate MCP, Skills, and CLI

Gate Skills Hub

10K+ Skills

From office tasks to trading, the all-in-one skill hub makes AI even more useful.

GateRouter

Smartly choose from 40+ AI models, with 0% extra fees

Historic Moment: Officially Takes Effect, NYSE Opens a New Era of Tokenized Securities

Article by: Shannon@Golden Finance

Tokenized stocks on the NYSE are really coming this time!

On May 12, 2026, the official website of the U.S. SEC published a document detailing the rule amendment proposal for tokenized securities previously submitted by the NYSE, and stated that the NYSE tokenized securities proposal has automatically taken effect.

U.S. SEC official document

This marks a milestone event where a traditional U.S. securities exchange officially incorporates blockchain technology into mainstream trading infrastructure.

Background: How did this happen?

The appearance of this document was not sudden. The entire policy pathway is clearly visible:

Step 1 (December 11, 2025): SEC staff issued a No-Action Letter to the Depository Trust Company (DTC), authorizing DTC to conduct a three-year pilot program for tokenized securities settlement (the “DTC Pilot Program”).

Step 2 (March 2026): Nasdaq applied for and received approval from the SEC for a similar rule, becoming the first major exchange to allow trading of tokenized securities.

Step 3 (May 1, 2026): NYSE National followed up by submitting this rule change application, and on May 12, the SEC issued an announcement, which automatically took effect in accordance with law.

The core legal basis for this rule change is Section 19(b)(1) of the Securities Exchange Act of 1934. NYSE National added Rule 7.39 and amended Rules 1.1, 7.36, 7.37, and 7.41 to establish a complete framework for trading tokenized securities.

Core Content: What does the rule specifically say?

What are “tokenized securities”?

The document clearly defines: Tokenized securities are digital representations of securities using distributed ledger or blockchain technology, contrasted with “traditional securities” (also digital representations but not using blockchain). Essentially, both represent the same asset; the difference lies in the underlying technology.

Which securities can be traded as tokenized securities?

The scope is strictly limited to two asset classes: one is Russell 1000 Index component stocks (the top 1,000 U.S. listed companies by market capitalization), and the other is ETFs tracking major indices. These two asset types are collectively called “DTC-qualified securities.”

What conditions must be met for tokenized securities to be listed and traded?

The document sets strict equivalency requirements: Tokenized securities must share the same CUSIP number and trading symbol as their traditional counterparts; holders must have identical rights (including equity rights, dividends, voting rights, and liquidation distributions); and they must be fully fungible in the market.

If the tokenized version does not meet these conditions, it will be considered a derivative or depositary receipt, not an equivalent security.

How does the trading mechanism work?

The process is quite straightforward. DTC-qualified participants wishing to settle via tokenization, when placing an order on the NYSE National system, select a “tokenization flag” and provide blockchain type and digital wallet address. The exchange will pass this preference to DTC after trade, and DTC will execute tokenized settlement. If participants are ineligible, securities do not meet conditions, or the wallet is incompatible with the DTC pilot, the order will automatically settle traditionally without error or interruption.

Which rules remain unchanged?

This is one of the most noteworthy parts—the vast majority of existing rules remain completely unchanged:

All order types and routing strategies apply as usual; tokenized and traditional securities are matched on the same order book with the same priority, and the tokenization flag does not affect trade priority; settlement remains T+1 (next-day settlement); fee schedules are indistinguishable between tokenized and traditional trades; market data does not differentiate between the two forms; FINRA’s market surveillance covers tokenized securities; obvious errors and risk management measures are equally applicable; and proxy voting distribution processes are essentially unchanged.

According to the document, the philosophy behind this change is to “utilize existing structures, participants, and rules,” rather than creating a new system.

Implementation and Regulatory Safeguards

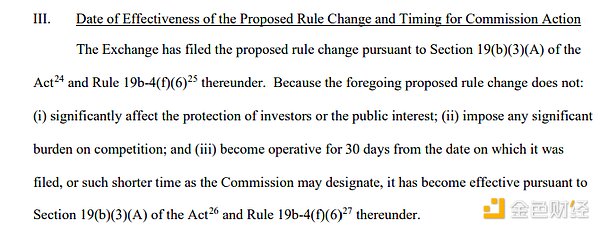

Because this rule change is deemed not to significantly impact investor protection or impose a substantial burden on competition, under Section 19(b)(3)(A) of the Securities Exchange Act, it automatically takes effect 30 days after submission without SEC formal approval or vote.

However, the SEC reserves the right: within 60 days of the document’s submission, if deemed necessary, it can temporarily suspend the rule change and initiate formal approval or rejection procedures.

The DTC pilot program is set for three years, after which NYSE National will reassess whether to extend or submit a new rule proposal.

Conclusion: The historical significance of this document

While the document appears highly technical, its significance is profound and can be understood on three levels:

For Wall Street: Blockchain technology officially enters the core infrastructure of mainstream U.S. securities trading. The Russell 1000 index represents the largest U.S. listed companies, plus major ETFs, meaning most trading volume in the market can be settled via tokenization.

For regulatory paradigm: The SEC has chosen a “no special track” approach—tokenized securities do not enjoy any exemptions, do not create parallel markets, and operate entirely within the existing national market framework. This is in stark contrast to prior market concerns about “regulatory arbitrage,” providing a reference model for regulators in other countries.

For the integration of crypto and traditional finance: Coupled with the U.S. Congress’s ongoing Clarity Act and the previously passed Genius Act, this SEC document signifies another direction of integration—where traditional finance actively incorporates blockchain technology, rather than crypto entering traditional finance. Both paths are advancing simultaneously and will eventually meet at a convergence point.

As the document states, this change is fundamentally similar to the transition from face value pricing to decimal quoting in securities, or the initial approval of ETFs—technological upgrades to market infrastructure that do not alter the core rules.