Futures

Access hundreds of perpetual contracts

CFD

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

CFD

U.S. stock CFD derivatives

US Stocks

Access real US stocks and ETFs

HK Stocks

Trade quality Hong Kong-listed stocks

Korean Stocks

SK Hynix

Real Korean stocks and top assets

Stock Futures

High leverage, 24/7 trading

Tokenized Stocks

Backed by real stock assets

IPO Access

Unlock full access to global stock IPOs

GUSD

Mint GUSD for Treasury RWA yields

Stocks Activities

Trade Popular Stocks and Unlock Generous Airdrops

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

IPO Access

Unlock full access to global stock IPOs

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

Promotions

AI

Gate AI

Your all-in-one conversational AI partner

Gate AI Bot

Use Gate AI directly in your social App

GateClaw

Gate Blue Lobster, ready to go

Gate for AI Agent

AI infrastructure, Gate MCP, Skills, and CLI

Gate Skills Hub

10K+ Skills

From office tasks to trading, the all-in-one skill hub makes AI even more useful.

Oracle: The Second Battlefield Behind the Prediction Market War

Author: Chloe, ChainCatcher

Over the past two years, prediction markets have become the brightest narrative in the crypto industry. The entire sector’s total trading volume at the end of last year approached $10 billion, with monthly growth momentum significantly accelerating in the second half of 2025.

But on the other end of this celebration, there is a role that has always stood outside the spotlight, repeatedly criticized harshly by users: oracles.

UMA’s Double-Edged Sword

In the past year, several major controversies surrounding Polymarket—such as the question of whether Ukrainian President Zelensky was wearing a suit (total trading volume of $237 million), Ukraine’s mineral rights agreement (involving $7 million, with a whale using about 5 million UMA to manipulate votes), and whether the Trump administration would declassify UFO files in 2025 (a $16 million market, publicly called a “whale proof” scam)—all trace back to the same source: UMA’s Optimistic Oracle and its token governance structure.

UMA’s Optimistic Oracle is designed so that anyone can propose an outcome, staking collateral; if no disputes are raised during the challenge period (usually 2 hours), the result is accepted as true; if disputed, UMA token holders vote via the Data Verification Mechanism (DVM) to decide.

This mechanism has obvious advantages: it’s cheap, capable of handling tail events, and can address “subjectivity issues,” such as whether Zelensky’s outfit counts as a suit—problems traditional price oracles cannot handle.

However, several controversies involving Polymarket have exposed flaws in this design. For example, the Ukraine mineral rights event in March last year, which involved about $7 million in trading volume, concerned whether Trump would reach a rare earth mineral agreement with Ukraine before April.

Although no agreement was reached, the market was settled as “Yes.” According to reports from The Defiant and Cryptopolitan, the main reason was a large UMA whale holding about 5 million UMA across three accounts, accounting for roughly 25% of the voting power in that round, pushing votes toward “Yes.” Subsequently, Polymarket publicly stated in Discord: “This is not a system malfunction but a result of governance operation, so refunds are refused.”

It can be said that Polymarket’s reliance on UMA is facing systemic risks. Originally designed as a “neutral truth arbitration layer,” the oracle’s concentrated token distribution now serves as a tool for a few to influence market outcomes.

Data from crypto asset data platform RootData shows that until September last year, when Polymarket began promoting crypto-related events, it urgently needed a more definitive data source, leading it to delegate some settlement work to another completely different oracle system: Chainlink.

Chainlink: Another Dilemma for the Industry Leader

CoinDesk reports that Polymarket started integrating Chainlink to improve its prediction result determination. Both parties announced that Polymarket would use Chainlink for automatic settlement of markets related to asset prices, reducing delays and tampering risks. Initially focusing on crypto asset price markets, they also explored applications in more subjective markets.

The significance of this partnership lies in that Polymarket, which previously relied on UMA’s “group consensus-based subjective arbitration,” now has a path to directly read market prices and automate decision-making through Chainlink.

Looking at the market landscape, Chainlink is undisputedly the leader in the oracle space, holding over 87% of the market cap in the oracle sector, with a TVS share of 61.58% (about $62.9 billion), far ahead of second-place Chronicle (10.15%) and third-place RedStone (7.94%).

It can also be said that its penetration into DeFi is nearly saturated. Major protocols—from Aave, GMX, Synthetix’s liquidation and pricing, to Curve’s security reference and Lido’s cross-chain standards—almost all utilize services provided by Chainlink.

Market share is reflected in its deployment. Chainlink provides around 2,000 price feeds on approximately 27 chains, and has deployed Data Streams (low-latency, on-demand high-frequency feeds) on 37 networks; its CCIP (Chainlink Cross-Chain Interoperability Protocol) mainnet covers 70 public chains and L2s, with about 200 cross-chain tokens registered under the CCIP standard.

This scale effectively transforms Chainlink from a “single-chain price intermediary” into a “multi-chain information and asset exchange layer.”

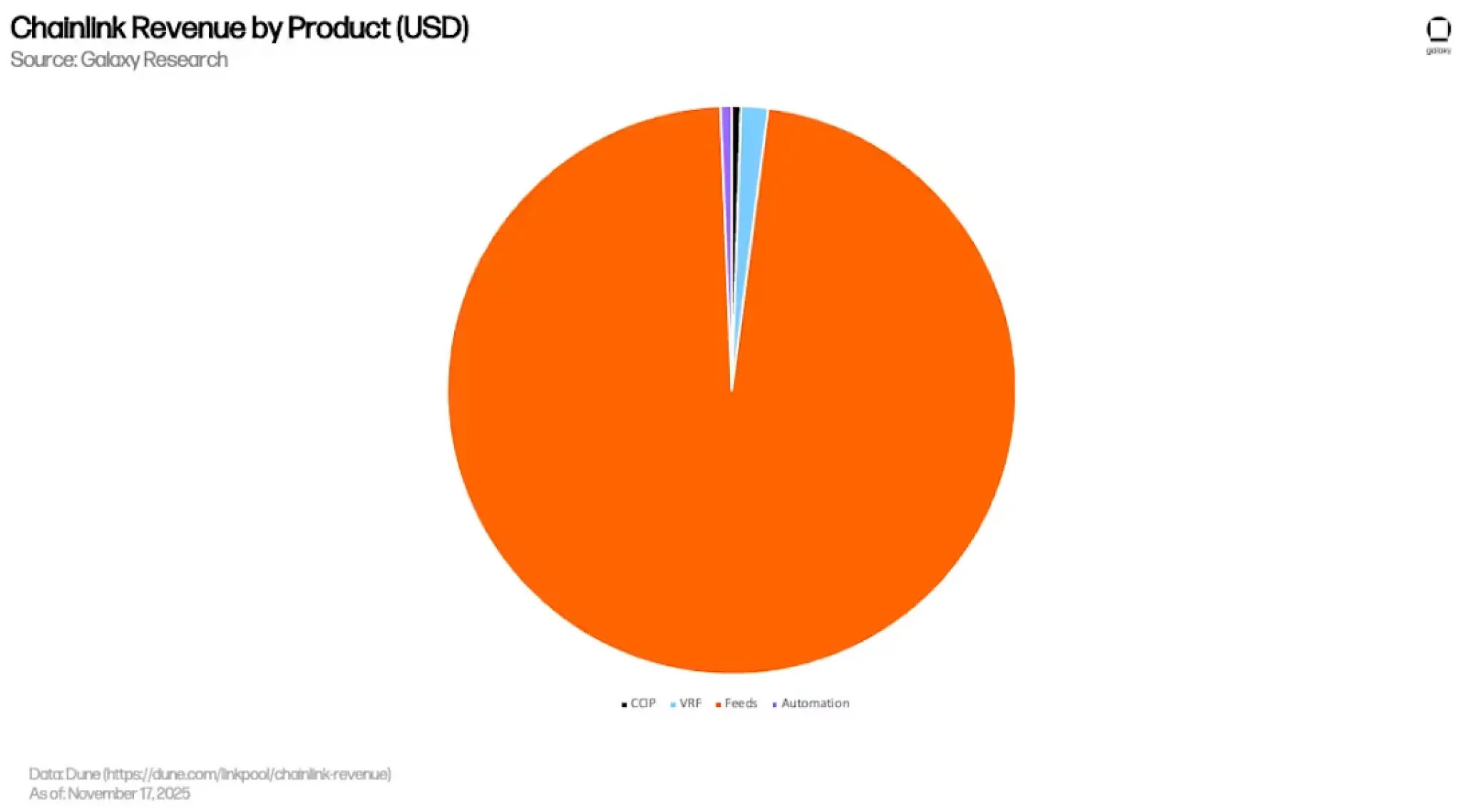

But saturation also means that DeFi is no longer its growth driver. According to Galaxy’s deep report, about 97% (roughly $399 million) of Chainlink’s total revenue comes from Price Feeds, while VRF (Verifiable Random Function, used for NFT minting and on-chain gaming), Automation, and CCIP account for only about 1.5%, 0.6%, and 0.5%, respectively.

**

**

**

In other words, Chainlink’s capital flow is highly concentrated in its most mature, commoditized price feed business, which has already reached market saturation, leaving very limited marginal growth potential.

In response, Chainlink is betting on three incremental growth paths.

The first is RWA and institutional finance.

From Chainlink’s partnership matrix, it’s clear that it has previously collaborated with Swift and several institutions to pilot cross-chain tokenized assets; last year, it worked with 24 major financial institutions to advance on-chain corporate actions data; the DTCC Smart NAV pilot has distributed mutual fund NAV data onto the chain.

In the same year, Chainlink partnered with Mastercard to enable on-chain crypto purchases for over 3 billion cardholders; the U.S. Department of Commerce (BEA) also integrated core macroeconomic data such as GDP and PCE into Chainlink Data Feeds, initially covering 10 public chains.

The second is CCIP cross-chain communication.

CCIP has become one of the preferred standards for cross-chain interoperability. JPMorgan’s Kinexys collaborated with Chainlink and Ondo to complete a cross-chain DvP settlement test for tokenized U.S. Treasuries; Aave is using it to promote GHO cross-chain, Lido has adopted it as the official cross-chain standard for wstETH; in the same year, CCIP launched on Aptos, extending its reach into the Move ecosystem.

By October 2025, CCIP had processed nearly $2 billion in token transfers.

The third is prediction markets and “event settlement financialization.”

Polymarket’s integration marks the beginning of this path. It signifies Chainlink’s expansion from serving only “asset prices” into the broader realm of “event settlement.” As prediction markets see exploding demand for automated settlement of asset classes like U.S. stocks, commodities, ETFs, and macro indicators, Chainlink finds a natural extension of its original price business here.

Overall, while Chainlink remains the market leader, growth in traditional DeFi price prediction oracles has peaked; it must rely on RWA, institutional finance, CCIP, and prediction market financialization to rebuild its next growth curve.

These potential growth paths are significant. According to BCG estimates, the tokenized RWA market could reach $16 trillion by 2030, and SWIFT processes about $150 trillion in settlements annually, but with settlement cycles measured in “years,” while token holders’ patience is often measured in “days.”

This mismatch may be the core pressure Chainlink faces as a leader in 2026.

Multiple Oracles Eroding the Prediction Market’s Big Pie

In early April, Polymarket announced a partnership with Pyth Network.

On this platform, prediction markets for short-term price movements of commodities like gold, silver, WTI crude oil, natural gas, as well as over ten U.S. stocks including NVDA, AAPL, TSLA, COIN, and PLTR, along with major indices and ETFs, will have settlement data provided in real-time via Pyth’s WebSocket, with sampling every second.

As a first-party data provider (with market makers and institutions like Jump Trading, Jane Street, Blue Ocean, LMAX directly publishing data), Pyth uses a pull model, enabling low-latency data delivery to applications.

This division of labor is not unique to Polymarket. Regulated by the U.S. CFTC, Kalshi has also integrated Pyth as its new commodity center’s settlement data source, covering gold, silver, Brent crude, natural gas, copper, corn, soybeans, wheat, and other commodities; Pyth Pro provides direct market data access to Kalshi’s market makers, with plans to expand to indices, stocks, and forex.

When both Polymarket and Kalshi choose Pyth as the settlement layer for traditional financial assets, it reflects a broader industry trend: the prediction market sector’s demand for “institution-grade high-frequency data settlement layers.”

Pyth has carved out a segment in this space, but it remains a subset of “traditional financial asset events,” separate from Chainlink’s focus on crypto assets and UMA’s subjective data.

This three-layer division reveals the current reality of the oracle industry as exposed by prediction markets.

First, no single oracle can fully serve a mature prediction market.

UMA’s community arbitration cannot handle high-frequency prices; Chainlink’s on-chain feeds are not optimal for millisecond-level event settlement; Pyth, while excellent for low-latency prices, cannot handle textual data at all.

Second, each new oracle introduced by Polymarket expands its “tradable event” universe.

From UMA’s non-standard events, to Chainlink’s crypto assets, to Pyth’s traditional financial assets, each step incorporates more real-world uncertainties into on-chain betting. Following this logic, future markets could include macroeconomic indicators (GDP, CPI, interest rate decisions), central bank rate announcements, corporate earnings, and even AI model releases.

As long as verifiable data sources exist, corresponding markets can be built.

Conversely, for oracle projects, this also means that prediction market expansion will not benefit any single oracle exclusively. Each new market will be allocated to the oracle best suited to handle that data type, leading to multi-party sharing and non-overlapping niches.

Conclusion

By 2026, the oracle sector has essentially evolved from an early “data pipeline” into a “verifiable facts layer” supporting the entire on-chain economy.

Its scope has expanded beyond DeFi liquidation and collateral valuation to include RWA compliance verification, cross-chain information transfer, and prediction market settlement of real-world uncertainties.

And prediction markets serve as a magnifying glass to observe this fiercely competitive landscape.

Polymarket’s three-track division, along with Kalshi’s parallel focus on traditional assets, reveals a stark reality: no single oracle can fully serve a mature on-chain application. Every topic on the platform will be assigned to the most suitable oracle for that data structure.

Infrastructure differentiation is now a fact. But when no single project can monopolize the benefits, who can truly become indispensable?