Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

More

Deep Dive: The Machine Payments Protocol

The financial infrastructure of the internet is being re-architected. On March 18, 2026, the launch of the Machine Payments Protocol (MPP) and the Tempo mainnet signaled the possible end of the human-centric checkout era. Actually, this could be a fundamental shift in how value moves across the web. For thirty years, the internet lacked a native value layer, forcing the industry to build increasingly complex user interfaces around legacy credit card rails. These interfaces, designed for human psychology, have become the primary bottleneck for the emerging agentic economy.

I believe the fundamental friction of the modern web is the “human-in-the-loop” requirement for commerce. AI agents do not use browsers. They do not click buttons, they do not solve CAPTCHAs, and they do not possess the cognitive friction that leads to cart abandonment. When an AI agent requires a resource, payment is a programmatic prerequisite for task completion; it is not a psychological preference. The Machine Payments Protocol, co-authored by Stripe and Tempo Labs, formalizes this reality by reviving the HTTP 402 “Payment Required” status code into a standardized, machine-readable challenge-response framework.

The failure of human-centric micropayments

There are three generations of failure in the micropayments graveyard. Every previous attempt failed because the assumed payer was a person. Humans calculate mental transaction costs for even the smallest payments. This leads to a hesitation that breaks the economics of digital content and services.

MPP succeeds where these failed because it eliminates the human decision point. For an agent, the cost of a transaction is a variable in an optimization function; it does not rely on an emotional event. This allows for sub-cent transaction models to finally become viable at scale.

MPP technical architecture

The core of MPP is its reliance on standard HTTP semantics, specifically the “Payment” HTTP Authentication Scheme proposed to the IETF. The protocol is a deterministic state machine that operates in a single round trip, removing the need for API keys or pre-existing accounts.

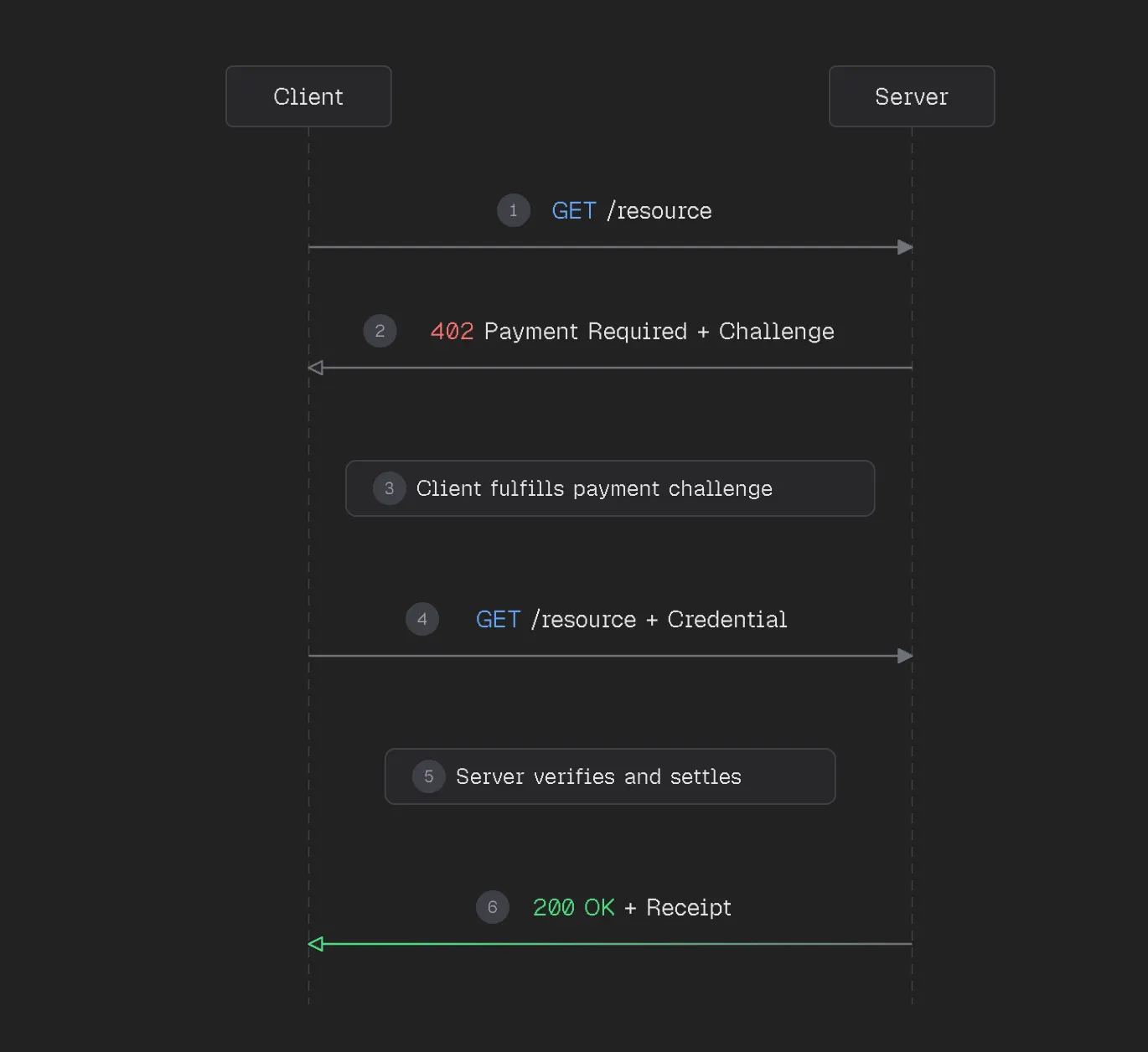

The five-step request-response cycle

The protocol operates through a formal sequence that embeds payment directly into the transport layer:

Resource Request: The agent initiates a standard request to a protected endpoint, such as POST /api/search.

Payment Challenge: The server intercepts the request and returns an HTTP 402 Payment Required status. The response includes a WWW-Authenticate: Payment header containing the payment challenge, which specifies the price, accepted currencies, and recipient address.

Payment Fulfillment: The MPP client fulfills the challenge by signing a transaction or authorizing a card-based token.

Credential Submission: The agent retries the request, attaching a signed payment credential in the Authorization: Payment header.

Resource Delivery: The server verifies the credential, settles the payment, and returns the resource along with a Payment-Receipt header.

Market implications for fintech and B2B

The shift to machine payments transforms the API from a developer tool into a high-throughput sales channel. This is a realization of Ronald Coase’s Transaction Cost Economics. By reducing the cost of negotiation and settlement to near-zero, we enable a more granular and efficient market for digital services.

The death of subscription dominance

The current model of monthly recurring revenue (MRR) is often a proxy for the high transaction costs of human checkout. If it costs $0.30 to process a credit card, you cannot charge $0.01 for a single API call. MPP and Tempo’s stablecoin settlement reduce per-transaction overhead to a fraction of a cent, making pay-per-use the dominant pricing model for the agent economy.

B2B procurement automation

In the B2B sector, procurement is already heavily software-driven. MPP creates a direct integration layer between a buyer’s procurement agents and a seller’s catalog, bypassing the need for manual purchase orders or bespoke EDI integrations. I expect this to accelerate the “long tail” of B2B commerce, where small, frequent transactions between machines replace large, occasional contracts negotiated by humans.

Strategic recommendations for the C-Suite

The Machine Payments Protocol is the catalyst for the next $3 to $5 trillion in global transaction volume. For fintech founders and CEOs, the path forward requires a transition from building human-readable interfaces to building machine-readable protocols.

I recommend four primary strategic pivots. First, eliminate interaction friction. If your service requires a human to create an account before an API can be called, you are invisible to the agent economy. Second, adopt multi-rail settlement. Integrate with infrastructure that supports both stablecoin and card-based rails to maximize your reachable market of agents. Third, implement economic firewalls. Governance is the prerequisite for production deployment. Fourth, optimize for token efficiency. Serve lightweight, data-only templates to agents to reduce their processing costs and ensure you are prioritized in their discovery workflows.

We are moving from an era where payments were an occasional interruption in a human’s browsing session to one where payments are the heartbeat of the internet’s autonomous actors. The infrastructure is ready. The protocol is live. The only remaining bottleneck is legacy thinking that continues to design for humans in a machine-driven world.

Disclaimer:

Fintech Wrap Up aggregates publicly available information for informational purposes only. Portions of the content may be reproduced verbatim from the original source, and full credit is provided with a “Source: [Name]” attribution. All copyrights and trademarks remain the property of their respective owners. Fintech Wrap Up does not guarantee the accuracy, completeness, or reliability of the aggregated content; these are the responsibility of the original source providers. Links to the original sources may not always be included. For questions or concerns, please contact us at sam.boboev@fintechwrapup.com.