Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

More

If Saudi Arabia's "Plan B" also fails to extend the port of Yanbu and the Strait of Mandeb, will oil prices rise another $20?

As Saudi Arabia shifts its crude oil export focus to the Red Sea to avoid the risks of the Strait of Hormuz, this “safe passage” itself is becoming a new eye of the storm.

According to the Chase Trading Desk, a report from JPMorgan on March 29 noted that the Houthis officially joined the Middle Eastern conflict, fundamentally changing the risk landscape of the global crude oil supply chain. Previously, the market focused on the Strait of Hormuz; now both the Red Sea and Bab-el-Mandeb Strait are simultaneously exposed to the threat of war, with risks stacking up in a dual-line scenario.

Saudi Arabia’s “detour plan” to avoid the Strait of Hormuz—an alternative export route centered around Yanbu Port—is facing a devastating blow, with approximately 4.8 million barrels per day of bypass capacity at risk. The report estimates that if key nodes are damaged, oil prices could rise by another $20 per barrel.

Conflict map expands: from a single chokepoint to a dual blockade

Previously, the Middle Eastern conflict was mainly focused around the Persian Gulf and the Strait of Hormuz, but with the Houthis’ formal involvement, the geopolitical front has significantly lengthened.

The geographical significance of this change is particularly critical: the two most important channels for global energy trade—the Strait of Hormuz and the Bab-el-Mandeb Strait—are now both exposed to potential threats. Both are strategic chokepoints that are difficult to bypass; the blockage of either will trigger systemic supply chain shocks. The simultaneous pressure on both channels means that the “detour option” is greatly reduced, and supply elasticity is sharply decreased.

The Houthis’ strike capability primarily covers the following targets, which together form key nodes for Saudi Arabia’s Red Sea exports—crude oil and refined products exported from Yanbu Port and Rabigh Port must pass through the Bab-el-Mandeb Strait to reach Asian markets:

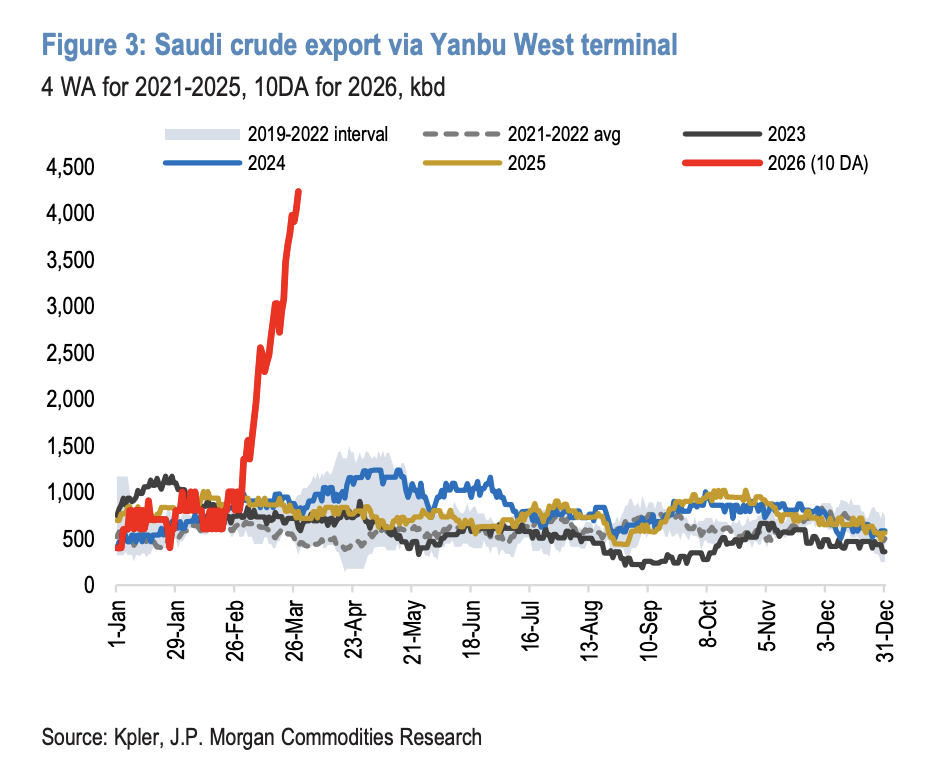

Yanbu Port: The Red Sea endpoint of the East-West Pipeline (Petroline), combining pipeline terminal and port functions, is Saudi Arabia’s main alternative crude oil export port;

Commercial shipping in the Bab-el-Mandeb Strait: The only navigable artery at the southern end of the Red Sea;

Rabigh Port: With an average daily export volume of about 200,000 barrels of refined products, it is also within potential strike range.

Saudi Arabia’s detour logic is being dismantled

Understanding the core of this risk lies in clarifying the “Hormuz alternative route” that Saudi Arabia previously constructed and the structural vulnerabilities it currently faces.

As the situation in the Strait of Hormuz continues to escalate, Saudi Arabia has massively shifted its crude oil export focus to Red Sea routes. Data shows that the amount of crude oil exported through Yanbu Port has surged from about 750,000 barrels per day to 4.3 million barrels per day, with an additional transfer potential of about 500,000 barrels per day, totaling nearly 4.8 million barrels per day of Red Sea export capacity now exposed to high risk. To support this shift, Saudi Arabia has deployed nearly 50 Very Large Crude Carriers (VLCCs) in the Red Sea, many of which are in waiting positions—forming a highly concentrated and clearly targeted fleet exposed to risk.

The crux of the issue lies here: when Saudi Arabia shifts oil to the Red Sea to avoid Hormuz risks, the involvement of the Houthis makes this “safe alternative route” itself a source of risk.

Limited backup options, significant logistics bottlenecks

If the Bab-el-Mandeb Strait faces substantial blockage, the daily 4.8 million barrels of crude oil exports from Yanbu Port will be forced to shift northward, relying on the Suez Canal and the SUMED pipeline to find an alternative route. In terms of the capacity of this backup path, estimates show:

SUMED Pipeline: Connecting Ain Sukhna in the Red Sea with Sidi Kerir in the Mediterranean, the theoretical maximum throughput capacity is 2.8 million barrels per day, but actual operations usually only reach about 1 million barrels per day. Even at full capacity, it cannot absorb the entire 4.8 million barrels shortfall.

Suez Canal: Approximately 2 to 2.2 million barrels per day of cargo would need to be diverted through the Suez Canal. However, Saudi crude oil exports heavily rely on VLCCs, which can only partially load when passing through the canal, meaning that either the number of trips must be significantly increased or smaller vessels must be used—both of which will raise transportation costs and delay deliveries.

Detour times will be significantly extended. If access to the Red Sea cannot be made directly through the Bab-el-Mandeb Strait, the round-trip journey to Asian markets will be extended by about 40 days, requiring an additional 130 tanker trips to maintain the normal shipping volume of 4.8 million barrels per day.

Oil price shock: could rise another $20 per barrel

If the aforementioned approximately 5 million barrels per day of Saudi detour capacity faces substantial threats, according to the bank’s estimates, it could exert upward pressure on oil prices of $20 per barrel. This increase corresponds to a scenario where detour capacity is forced to be interrupted, and supply cannot be promptly supplemented through alternative routes.

It is worth noting that this $20 upside risk is not based on the extreme assumption of Iran completely halting exports, but rather specifically targets the localized impact of disruptions to Saudi Arabia’s Red Sea export routes—indicating that the current magnitude of risk should not be underestimated.

Is escalation just a matter of time?

Will the Houthis choose to directly strike Saudi infrastructure and shipping routes, or will they retain this capability as a strategic bargaining chip for flexible use during the evolution of the conflict?

Analysts say that the issue of escalation has shifted from “will it happen” to “when will it happen.” As the conflict may further spread toward Iran (including larger-scale involvement of the Gulf Cooperation Council, strikes against Iranian infrastructure, and even the possibility of ground operations), with each passing day, the risk of escalation accumulates.

For energy market investors, this means that the current pricing of geopolitical risk premiums may still be insufficient, and the hedging value against the tail risk of rising oil prices is significantly increasing. The allocation logic of the energy sector, as well as the supply chain security assessments of global shipping and refining companies, need to be re-evaluated within this framework.