#BTCBreaks66000

Bitcoin is back above $66,000—and the breakout is attracting renewed attention across the crypto market.

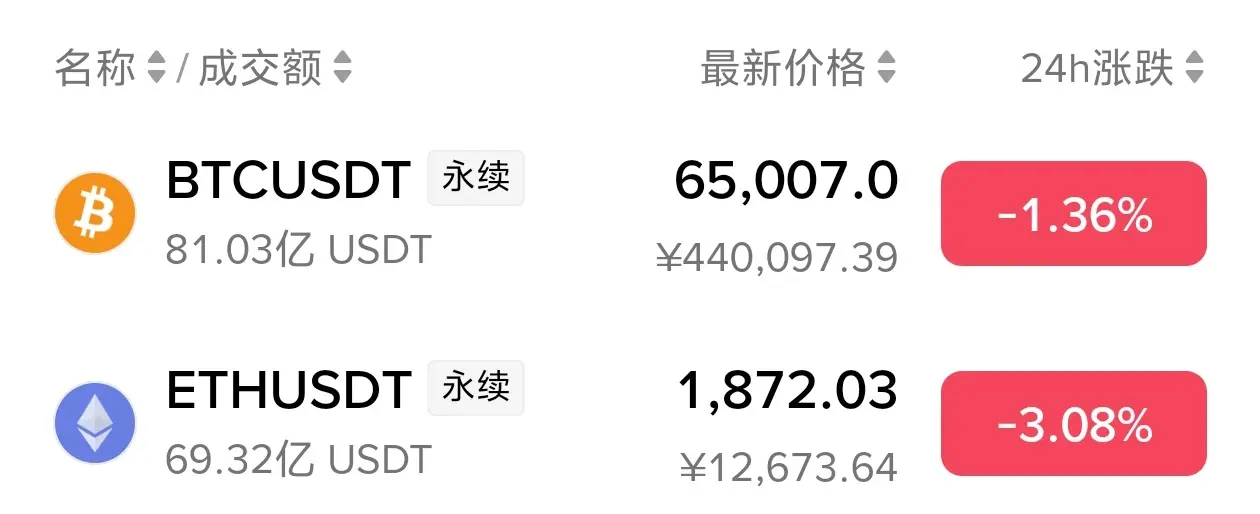

After weeks of consolidation and uncertainty, Bitcoin has reclaimed the $66,000 level, marking its strongest recovery in more than a month. The move represents a gain of over 3% in 24 hours and nearly 15% from July's lows, signaling that bullish momentum is gradually returning to the market.

What's driving this rally?

The biggest catalyst is the return of institutional demand. Spot Bitcoin ETFs have recorded strong inflows, showing that large investors continue to accumulate exposure despite recent market volatility. Institutional capital has historically played a key role in strengthening long-term market confidence, and the latest inflow data suggests that sentiment is improving once again.

Another important factor is the improving regulatory environment. Progress surrounding crypto legislation, including developments related to the CLARITY Act, has increased optimism that clearer regulatory frameworks could encourage broader institutional participation and support long-term industry growth.

From a technical perspective, Bitcoin has broken above a key descending trendline that had limited price action for several weeks. Reclaiming $66,000 shifts market sentiment in favor of the bulls and places the next major resistance zone around $67,400–$68,000. A sustained move above this range could strengthen momentum and potentially trigger another wave of buying.

However, experienced traders also recognize that breakouts require confirmation.

Trading volume has not expanded at the same pace as price, suggesting that market participants should remain cautious. Summer trading conditions often bring lower liquidity, making price movements more volatile and increasing the possibility of false breakouts or short-term pullbacks.

The coming sessions will therefore be crucial. If Bitcoin successfully holds above $66,000, buyers may gain additional confidence and target higher resistance levels. On the other hand, failure to maintain this support could lead to profit-taking before the next directional move.

Beyond short-term fluctuations, Bitcoin's broader investment thesis continues to strengthen. Institutional adoption, expanding ETF participation, improving regulatory clarity, and increasing global acceptance continue to support its position as the world's leading digital asset.

For investors, the message remains simple: price movements create headlines, but fundamentals build long-term value. Markets will always experience periods of volatility, yet disciplined investors focus on risk management, market structure, and long-term trends rather than reacting emotionally to every candle.

Bitcoin has cleared an important milestone—but the real test begins now. The market will be watching closely to see whether this breakout becomes the foundation for the next bullish phase or simply another temporary rally.

#BTCBreaks66000 #Bitcoin #Crypto #GateSquare

Bitcoin is back above $66,000—and the breakout is attracting renewed attention across the crypto market.

After weeks of consolidation and uncertainty, Bitcoin has reclaimed the $66,000 level, marking its strongest recovery in more than a month. The move represents a gain of over 3% in 24 hours and nearly 15% from July's lows, signaling that bullish momentum is gradually returning to the market.

What's driving this rally?

The biggest catalyst is the return of institutional demand. Spot Bitcoin ETFs have recorded strong inflows, showing that large investors continue to accumulate exposure despite recent market volatility. Institutional capital has historically played a key role in strengthening long-term market confidence, and the latest inflow data suggests that sentiment is improving once again.

Another important factor is the improving regulatory environment. Progress surrounding crypto legislation, including developments related to the CLARITY Act, has increased optimism that clearer regulatory frameworks could encourage broader institutional participation and support long-term industry growth.

From a technical perspective, Bitcoin has broken above a key descending trendline that had limited price action for several weeks. Reclaiming $66,000 shifts market sentiment in favor of the bulls and places the next major resistance zone around $67,400–$68,000. A sustained move above this range could strengthen momentum and potentially trigger another wave of buying.

However, experienced traders also recognize that breakouts require confirmation.

Trading volume has not expanded at the same pace as price, suggesting that market participants should remain cautious. Summer trading conditions often bring lower liquidity, making price movements more volatile and increasing the possibility of false breakouts or short-term pullbacks.

The coming sessions will therefore be crucial. If Bitcoin successfully holds above $66,000, buyers may gain additional confidence and target higher resistance levels. On the other hand, failure to maintain this support could lead to profit-taking before the next directional move.

Beyond short-term fluctuations, Bitcoin's broader investment thesis continues to strengthen. Institutional adoption, expanding ETF participation, improving regulatory clarity, and increasing global acceptance continue to support its position as the world's leading digital asset.

For investors, the message remains simple: price movements create headlines, but fundamentals build long-term value. Markets will always experience periods of volatility, yet disciplined investors focus on risk management, market structure, and long-term trends rather than reacting emotionally to every candle.

Bitcoin has cleared an important milestone—but the real test begins now. The market will be watching closely to see whether this breakout becomes the foundation for the next bullish phase or simply another temporary rally.

#BTCBreaks66000 #Bitcoin #Crypto #GateSquare