Artificial intelligence is propelling the global semiconductor industry into a new growth cycle. As demand for large model training, generative AI, and cloud computing continues to expand, the market for high-performance GPUs, high-speed networking, and advanced storage systems is growing in tandem. In the AI compute ecosystem, memory has evolved beyond a simple data storage function to become a critical infrastructure that determines system efficiency.

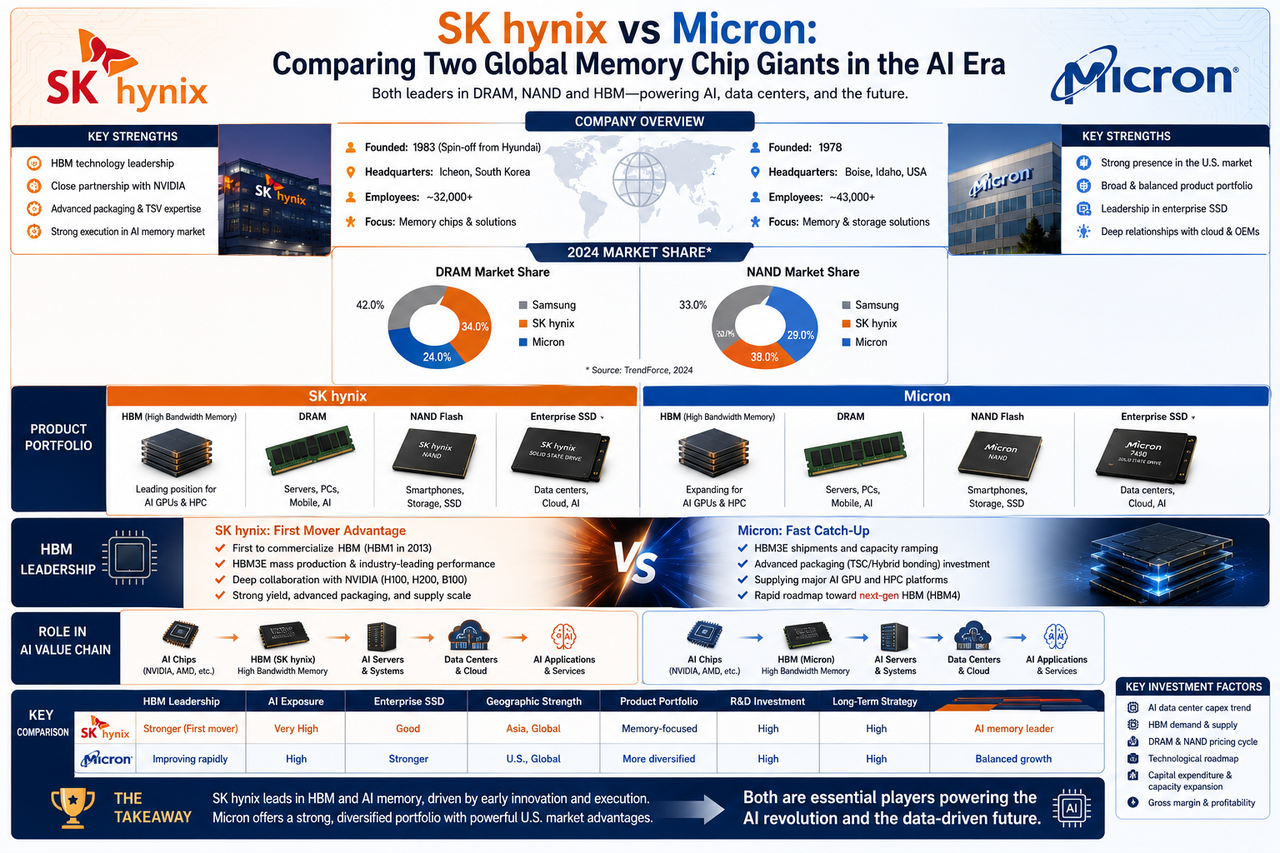

SK hynix and Micron Technology are major players in the global memory industry and key beneficiaries of the AI era. The two companies compete intensely across DRAM, NAND Flash, and HBM markets, while jointly contributing to global data center and AI infrastructure buildout. Although their business directions are similar, they differ significantly in technology roadmaps, market strategies, and industry ecosystems.

Who Dominates the Global Memory Chip Market?

The memory chip industry demands high technical barriers and substantial capital investment, resulting in a persistently high level of market concentration.

Currently, the global DRAM and NAND markets are primarily dominated by three companies: Samsung Electronics, SK hynix, and Micron Technology. Among them, Samsung holds the largest market share, while SK hynix and Micron compete fiercely across multiple segments.

Overview of the Three Major Global Memory Manufacturers

| Company |

Headquarters |

Core Products |

Market Position |

| Samsung Electronics |

South Korea |

DRAM, NAND, HBM |

Comprehensive semiconductor leader |

| SK hynix |

South Korea |

DRAM, NAND, HBM |

Leading AI memory provider |

| Micron Technology |

United States |

DRAM, NAND, HBM |

U.S. memory leader |

Together, these three companies command the vast majority of global DRAM market share and control the trajectory of advanced memory technology development.

What Is Micron?

Micron Technology, founded in 1978 and headquartered in Idaho, USA, is one of the largest memory chip manufacturers in the United States.

The company’s portfolio spans DRAM, NAND Flash, SSDs, and data center storage solutions, with products widely deployed in servers, smartphones, automotive electronics, and industrial equipment.

As a flagship enterprise of the U.S. semiconductor industry, Micron has long competed in the global memory market and holds significant influence in enterprise storage and data center segments.

What Are the Key Business Differences Between SK hynix and Micron?

From a product structure standpoint, both companies cover DRAM, NAND, and SSD markets, but their strategic focus diverges.

In recent years, SK hynix has channeled more resources into HBM and AI memory markets, aiming to strengthen its competitive edge through AI compute expansion. Micron, meanwhile, maintains robust competitiveness in enterprise storage, automotive memory, and the domestic U.S. data center market.

Business Comparison: SK hynix vs. Micron

| Dimension |

SK hynix |

Micron Technology |

Market Position |

| Core Markets |

AI servers, data centers |

Enterprise storage, data centers |

Comprehensive semiconductor leader |

| DRAM Business |

Global leader |

Global leader |

Leading AI memory provider |

| NAND Business |

Major revenue contributor |

Major revenue contributor |

U.S. memory leader |

| HBM Strategy |

Early mover |

Rapidly catching up |

|

| Geographic Advantage |

South Korean semiconductor ecosystem |

U.S. semiconductor ecosystem |

|

Overall, SK hynix benefits more from AI infrastructure expansion, while Micron maintains a more balanced business portfolio.

Why Has HBM Become a Competitive Flashpoint?

HBM (High Bandwidth Memory) is a critical component of AI chips and one of the most closely watched technology trends in the memory industry.

Modern AI GPUs must handle enormous data volumes, and traditional DRAM can no longer meet bandwidth requirements. HBM, leveraging 3D stacking and advanced packaging, dramatically increases bandwidth while reducing power consumption, making it essential infrastructure for AI compute systems.

With the explosive growth of generative AI, the HBM market has rapidly emerged as a core battleground for memory manufacturers.

Why Does SK hynix Hold an Edge in the HBM Market?

SK hynix was among the first companies globally to drive HBM commercialization.

Long before the AI boom, the company had already completed R&D across multiple HBM generations and continuously optimized TSV, advanced packaging, and mass production processes. When AI GPU demand for HBM surged, SK hynix possessed mature technology and production capacity.

This first-mover advantage has enabled SK hynix to build a strong competitive moat in the AI memory market and become a key participant in the AI GPU ecosystem.

HBM Competitiveness Comparison

| Comparison Item |

SK hynix |

Micron |

| HBM R&D Start |

Early |

Relatively late |

| AI Ecosystem Involvement |

High |

Rapidly rising |

| Packaging Experience |

Extensive |

Continuously strengthening |

| Market Recognition |

High |

Medium-high |

| AI Business Benefit |

High |

High |

How Is Micron Competing in the AI Memory Market?

In response to the AI market opportunity, Micron is aggressively expanding its HBM product lineup.

In recent years, Micron has launched next-generation HBM products targeting AI GPUs and high-performance computing platforms, while intensifying R&D in advanced packaging. At the same time, the company leverages its DRAM and SSD product lines to support data center construction.

Although it started later than SK hynix, Micron—drawing on its technological expertise and U.S. market advantages—is rapidly strengthening its position in the AI memory market.

Which Company Holds a More Important Position in the AI Value Chain?

From an industry chain perspective, both companies are essential pillars of AI infrastructure.

SK hynix focuses more on supplying high-bandwidth memory solutions for AI GPUs, giving it a tighter link to AI compute expansion. Micron, by contrast, covers enterprise storage, data centers, automotive electronics, and more, resulting in a more diversified business structure.

Role Comparison in the AI Value Chain

| AI Segment |

SK hynix |

Micron |

| HBM Supply |

Core participant |

Important participant |

| Data Center DRAM |

Core participant |

Core participant |

| Enterprise SSDs |

Important participant |

Core participant |

| AI Servers |

Deeply involved |

Deeply involved |

| Automotive Memory |

Emerging presence |

Strong advantage |

Thus, the two companies' relative importance varies by segment rather than being a straightforward comparison of dominance.

Who Has Greater Growth Potential in the AI Era?

AI infrastructure investment is a major growth engine for the memory industry.

If AI GPU and data center buildout continue to accelerate, the HBM market is poised for rapid growth. Under this scenario, companies with HBM technology advantages are likely to capture more upside.

At the same time, enterprise storage, cloud computing, and automotive electronics markets offer long-term expansion opportunities, giving Micron’s diversified business model certain advantages.

The future growth of both companies will largely depend on the pace of AI compute expansion, HBM technology iteration, and shifts in the global semiconductor cycle.

What Indicators Should Investors Watch?

When analyzing SK hynix and Micron, investors typically monitor the following metrics:

-

DRAM and NAND market pricing trends

-

HBM product shipment volumes

-

AI data center capital expenditures

-

GPU market growth

-

Semiconductor inventory cycles

-

Gross margins and R&D spending levels

These factors directly influence each company's future financial performance and competitive standing.

Summary

SK hynix and Micron Technology are key leaders in the global memory industry and major beneficiaries of AI infrastructure development. Both companies possess strong competitiveness in DRAM, NAND Flash, SSDs, and HBM markets, and jointly drive the evolution of AI memory technology.

In the AI era, HBM has become a critical technology shaping the competitive landscape. SK hynix has built a leading position through early investment and mature mass production capabilities, while Micron is rapidly closing the gap by leveraging its U.S. market strength and technological expertise.

FAQs

What Does Micron Do?

Micron Technology is a U.S. semiconductor company that manufactures memory products including DRAM, NAND Flash, SSDs, and HBM, widely used in data centers, smartphones, automotive electronics, and AI infrastructure.

Which Is Bigger: SK hynix or Micron?

From a global memory market perspective, both are industry leaders. SK hynix holds a stronger position in HBM and AI memory, while Micron is highly competitive in the U.S. market and enterprise storage segments.

Why Does HBM Affect the Competitive Landscape Between the Two Companies?

HBM is a critical component of AI GPUs. As AI compute demand grows, the HBM market expands rapidly, making it a key determinant of future memory industry competitiveness.

What Advantages Does SK hynix Have in HBM?

SK hynix invested early in HBM technology R&D and has accumulated extensive experience in advanced packaging and mass production, giving it a strong competitive edge in the AI memory market.

Is Micron Involved in the AI Value Chain?

Yes. Micron participates in AI infrastructure through HBM, DRAM, SSDs, and data center storage products, making it an important part of the global AI value chain.

What Should Investors Focus on When Investing in SK hynix and Micron?

Investors typically monitor AI data center construction, HBM market demand, DRAM and NAND pricing cycles, corporate R&D investment, and the overall global semiconductor industry cycle.