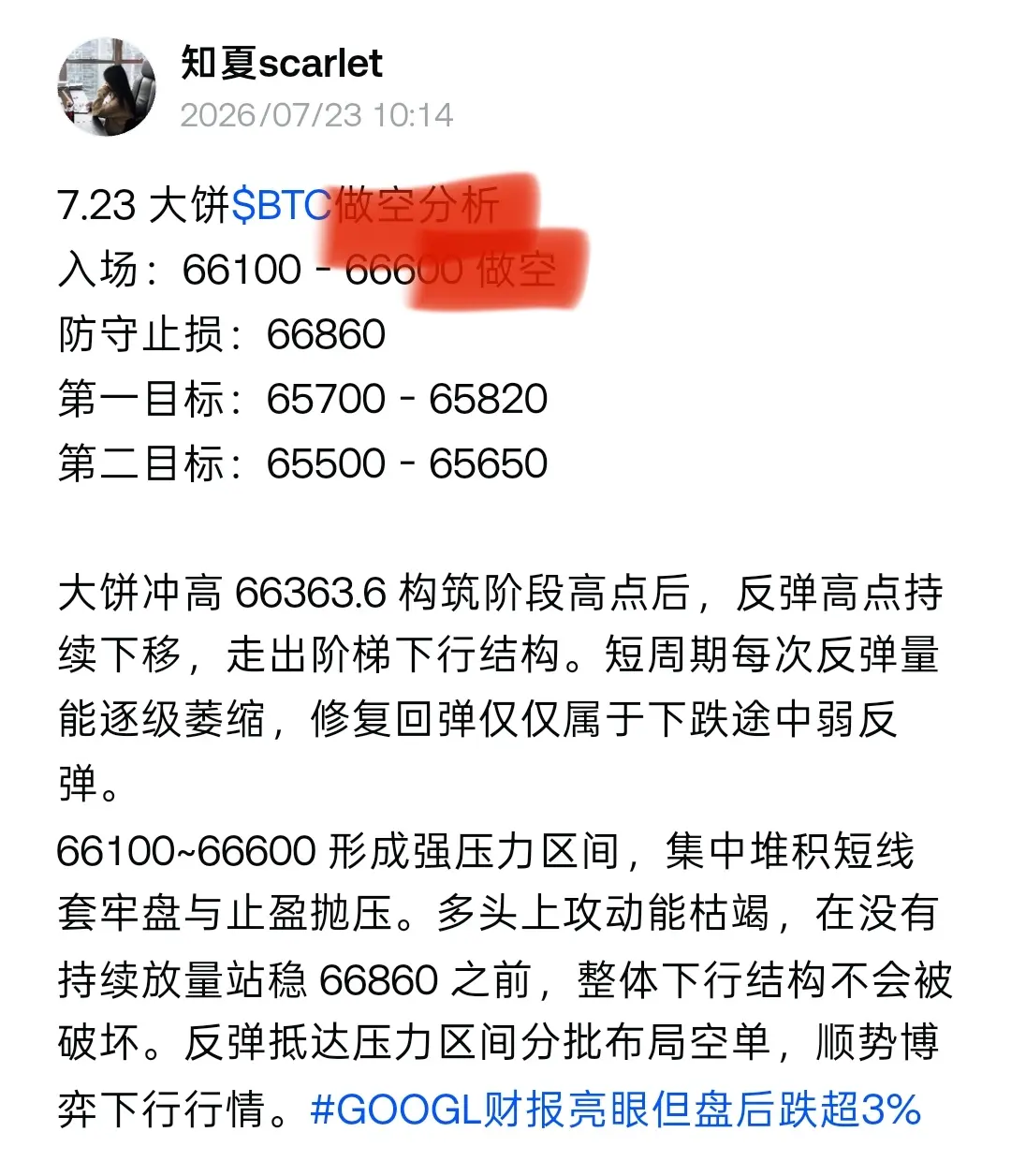

#GOOGL财报亮眼但盘后跌超3% Google’s 2026 Q2 earnings report may have exceeded expectations significantly on both revenue ($119.8 billion) and its cloud business ($24.8 billion, +82% year over year), but the after-hours stock price still fell by more than 3%. The core reasons are the “expectations gap” in the report and the market’s concerns about future profitability and cash flow. The specific reasons are as follows: 1. Doubts about the “quality” of net profit (one-off gains mask underlying weakness in the core business)

The earnings report shows net profit surged 294% year over year to $112.1 billion, but about $71.4 billion of that came from one-off equity investment gains (mainly paper gains from Anthropic and SpaceX), not from core operating profit.

·After excluding one-off gains, core operating EPS was only about $2.90-$3.00, slightly above expectations, failing to meet the market’s expectation of “explosive” growth.

2. Capital expenditures surge and free cash flow turns negative (worry over burn rate)

Q2 capital expenditures for the quarter reached $44.9 billion, doubling year over year, and the full-year Capex guidance was raised sharply to $195.0-$205.0 billion, indicating that investment in an AI arms race continues to expand.

Because the major Capex outlay consumes cash flow, free cash flow for the quarter turned to -$5.86B in Q2, the first time since Alphabet’s listing. The market worries whether such heavy investment can translate into profits in the near term, raising doubts about the sustainability of “burning cash for growth.”

3. Core business “Search” growth slows (a subtle concern in the base business)

Search business (including search ads) revenue was $63.3 billion, up 17% year over year, slightly below market expectations ($63.4 billion). Some institutions also point out that search growth may slow due to the high base.

The market originally had high expectations for a “Search + Cloud” dual-engine drive, and the relative weakness in the Search business to a certain extent dampened market sentiment. 4. Core AI model delayed (growth expectations take a hit)

The market expected the frontier AI large model Gemini 3.5 Pro, but it was delayed for reasons, and combined with AI talent loss, it raised concerns about whether its full-stack AI advantages can continue to lead and about the pace of AI commercialization.

5. Valuation has partially “Price in” (good news fully reflected)

Alphabet’s high revenue growth and cloud business growth were already partially reflected in the stock price before the earnings release. In after-hours trading, the market focuses more on “incremental negative factors” (such as negative cash flow and Capex exceeding expectations), leading to profit-taking and a reversal of sentiment in after-hours trading.

In summary, the “impressively strong” surface of Google’s earnings failed to fully offset the market’s concerns about its “high investment, low short-term returns.” Combined with some core metrics falling short of expectations, this led to downward pressure on the stock price in after-hours trading. #夏日创作营

The earnings report shows net profit surged 294% year over year to $112.1 billion, but about $71.4 billion of that came from one-off equity investment gains (mainly paper gains from Anthropic and SpaceX), not from core operating profit.

·After excluding one-off gains, core operating EPS was only about $2.90-$3.00, slightly above expectations, failing to meet the market’s expectation of “explosive” growth.

2. Capital expenditures surge and free cash flow turns negative (worry over burn rate)

Q2 capital expenditures for the quarter reached $44.9 billion, doubling year over year, and the full-year Capex guidance was raised sharply to $195.0-$205.0 billion, indicating that investment in an AI arms race continues to expand.

Because the major Capex outlay consumes cash flow, free cash flow for the quarter turned to -$5.86B in Q2, the first time since Alphabet’s listing. The market worries whether such heavy investment can translate into profits in the near term, raising doubts about the sustainability of “burning cash for growth.”

3. Core business “Search” growth slows (a subtle concern in the base business)

Search business (including search ads) revenue was $63.3 billion, up 17% year over year, slightly below market expectations ($63.4 billion). Some institutions also point out that search growth may slow due to the high base.

The market originally had high expectations for a “Search + Cloud” dual-engine drive, and the relative weakness in the Search business to a certain extent dampened market sentiment. 4. Core AI model delayed (growth expectations take a hit)

The market expected the frontier AI large model Gemini 3.5 Pro, but it was delayed for reasons, and combined with AI talent loss, it raised concerns about whether its full-stack AI advantages can continue to lead and about the pace of AI commercialization.

5. Valuation has partially “Price in” (good news fully reflected)

Alphabet’s high revenue growth and cloud business growth were already partially reflected in the stock price before the earnings release. In after-hours trading, the market focuses more on “incremental negative factors” (such as negative cash flow and Capex exceeding expectations), leading to profit-taking and a reversal of sentiment in after-hours trading.

In summary, the “impressively strong” surface of Google’s earnings failed to fully offset the market’s concerns about its “high investment, low short-term returns.” Combined with some core metrics falling short of expectations, this led to downward pressure on the stock price in after-hours trading. #夏日创作营