Gate Ventures Research Insights: Strategy-Based Synthetic Stablecoins — Building Financial Lego with Interest Rates

Gate Ventures

TL;DR

Stablecoins have long been regarded as the “crown jewel of the cryptocurrency industry,” but early development was primarily focused on algorithmic stablecoins, such as Ampleforth’s AMPL and Terra’s UST (LUNA). These projects sought to move away from reliance on U.S. dollar assets by using algorithmic mechanisms to construct encapsulated “dollar stablecoins,” with the goal of driving large-scale adoption of stablecoins within the crypto and DeFi ecosystems, and eventually expanding to traditional off-chain users. Beyond this shared ambition, the two projects also took notably different paths. Ampleforth aimed to create a native unit of settlement entirely belonging to the crypto world, and therefore did not maintain a strict 1:1 peg with the U.S. dollar. By contrast, TerraUSD (UST) attempted to maintain a stable peg to the dollar in order to serve more broadly as a payment method and a store of value.

This year, with the emergence of Ethena, DeFi stablecoins are no longer solely pegged to price stability but have begun to anchor themselves to “sources of yield.” A new category of “strategy-based stablecoins” is rising. Essentially, these tokens package hedging strategies or low-risk yield products into a $1-denominated transferable asset. For example, Ethena’s USDe functions much like a fund share. Behind it lies a delta-neutral strategy that goes long on stETH while shorting perpetual contracts to generate yield, which is then distributed to holders in the form of sUSDe. Because this stablecoin structure closely resembles subscription shares in a hedge fund, regulators such as BaFin in Germany have classified it as a security.

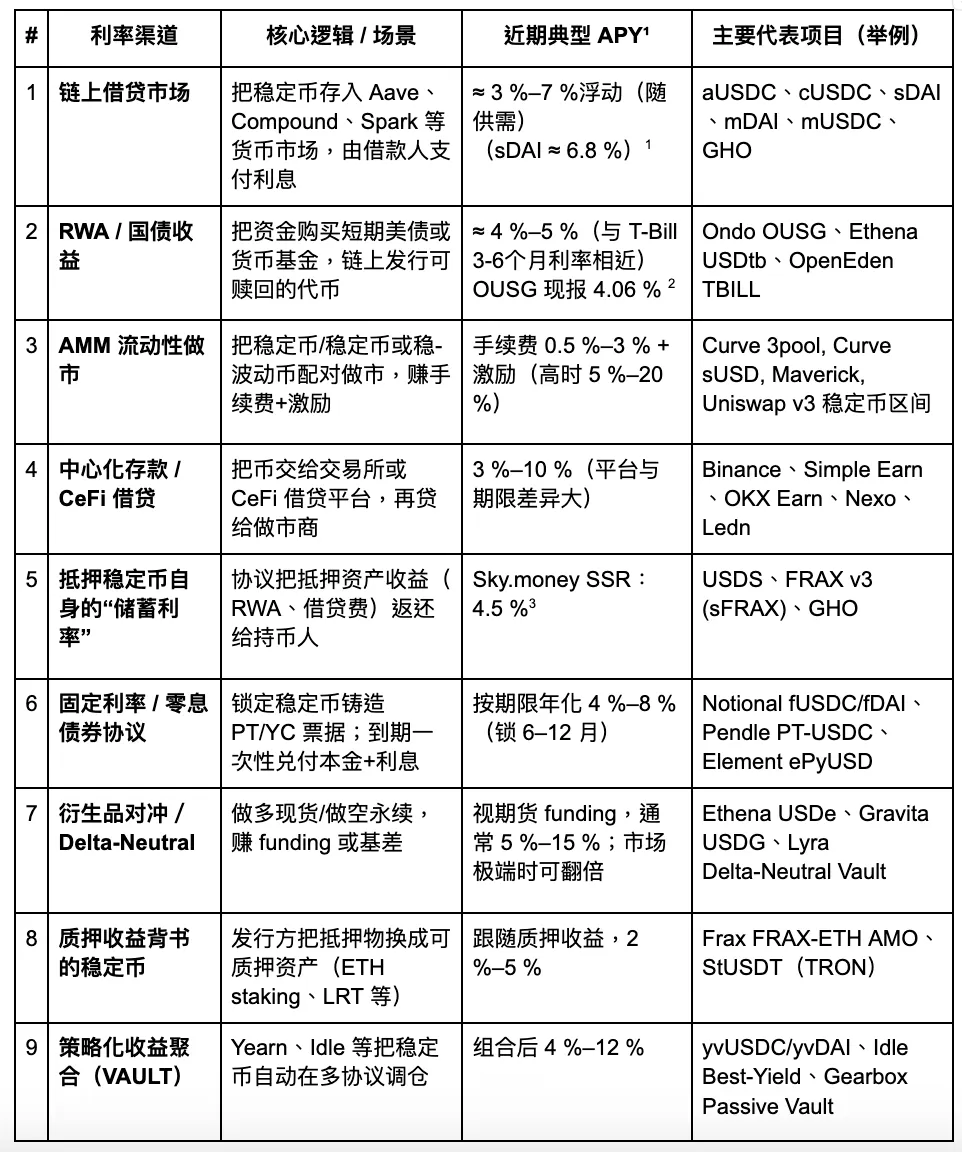

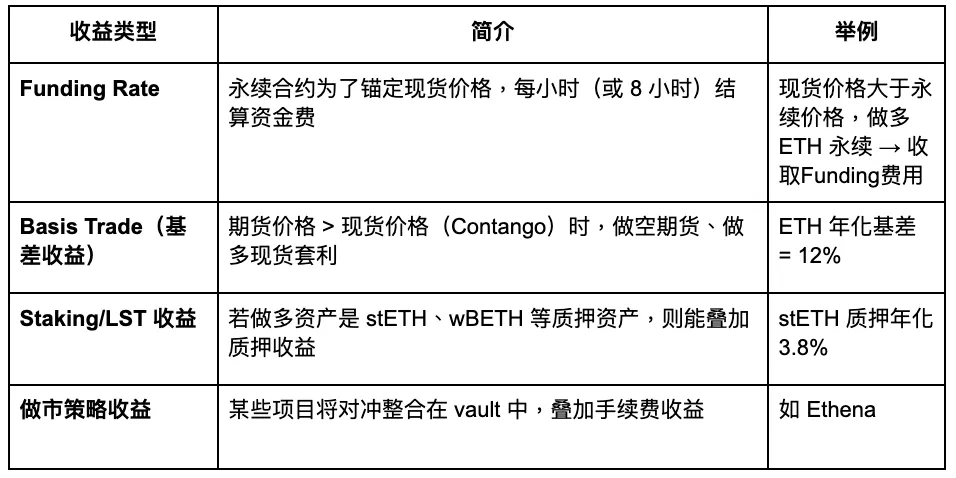

When systematically reviewing the yield mechanisms behind stablecoins, the article classifies them into nine main categories: on-chain lending, real-world assets (RWA), AMM market-making, CeFi deposits, protocol savings rates (such as DSR), fixed-rate notes, derivative hedging, staking yields, and strategy aggregation vaults. Across current market conditions, the annualized yields of these channels generally fall within the 3–8% range, though in special periods (such as during a USDC depeg or when funding rates surge), returns can briefly exceed double digits.

Although today’s strategy-based stablecoin projects may appear highly homogeneous on the surface, their core differences lie in three key dimensions: the sustainability of their yield structures, the transparency of their yield disclosures, and whether they are built on a foundation of regulatory compliance. Currently, stablecoins backed by real-world assets (RWA), such as USDY and OUSG, hold a relative advantage in compliance, having received a certain degree of regulatory recognition. However, their growth ceiling is constrained by the structural limits of the U.S. Treasury market. In contrast, derivative-linked stablecoins like USDe offer greater flexibility and yield potential, but they are also more dependent on the open interest (OI) in perpetual futures markets, making them significantly more sensitive to market volatility.

Within this trend, the biggest beneficiary among infrastructure projects is Pendle. The protocol decomposes yield-bearing assets into Principal Tokens (PT) and Yield Tokens (YT), thereby building an on-chain interest rate market and driving the standardization of “spread hedging” and “yield transfer.” As more and more stablecoin projects adopt Pendle to manage their cash flows, its TVL, trading volume, and bribe mechanisms are expected to see further growth.

We believe that the future of strategy-based stablecoins will evolve toward being modular, regulation-friendly, and yield-transparent. Projects that feature unique yield sources, robust redemption mechanisms, and liquidity moats through ecosystem adoption are likely to become the foundation for the next generation of “on-chain money market funds.” However, such products may still be classified as securities by regulators, and the potential compliance challenges should not be overlooked.

Strategy-Based Stablecoins

Yield-bearing stablecoins draw from multiple income channels, including lending protocols, liquidity mining, market-neutral arbitrage, RWA U.S. Treasury yields, structured option products, diversified stablecoin baskets, and staking rewards from stablecoins. Below is a summary of some of these yield strategies:

Gate Ventures

We will take a closer look at some of the key interest rate channels that feature notable innovations, along with their current status and potential catalysts, in order to assess their future development prospects.

On-Chain Lending Market

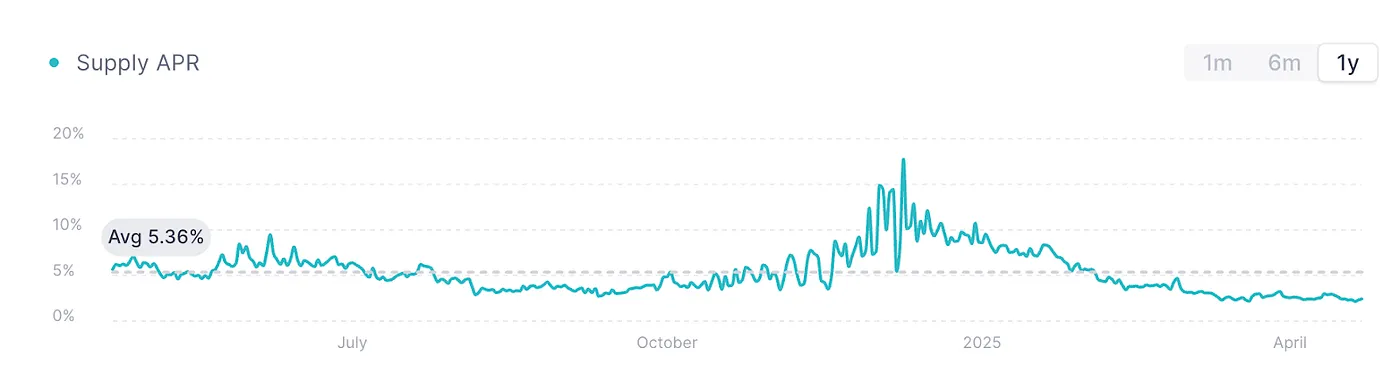

AAVE V3 USDC, source: AAVE

The chart above shows the USDC lending rate on AAVE V3’s Ethereum mainnet, which is generally regarded as the “benchmark rate” for on-chain lending. Amid weak market sentiment and insufficient demand for capital, lending activity has dropped significantly, causing rates to remain at a relatively low level of around 2% since the beginning of the year.

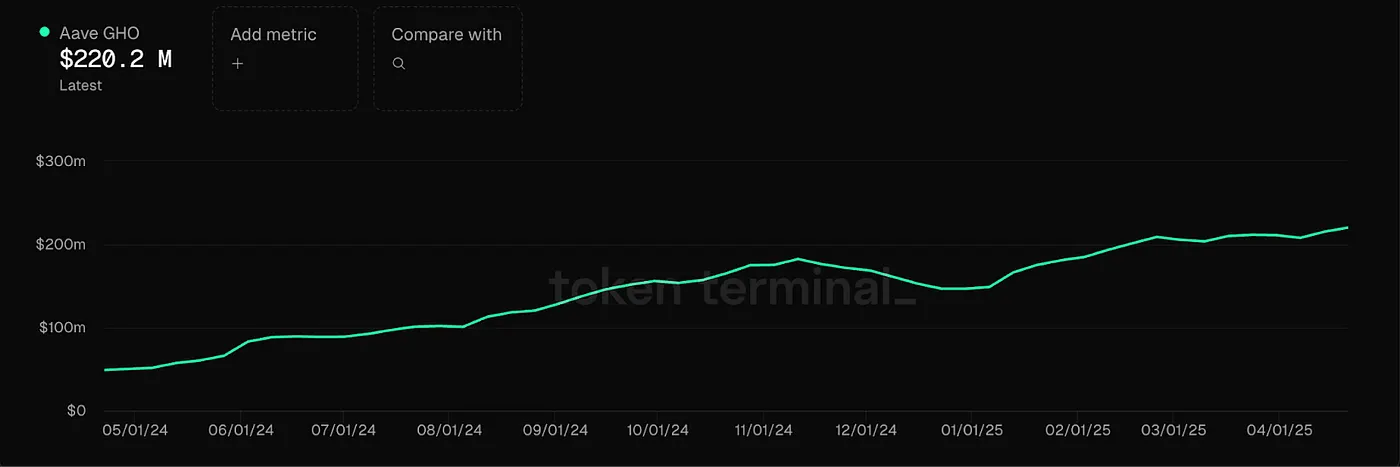

At the same time, AAVE has launched its native stablecoin GHO, supported by an overcollateralization mechanism, with its interest rate also determined by market lending demand. Although most mainstream stablecoins on this platform can generate interest, it must be done through lending, which limits capital efficiency. Currently, the borrowing rate for GHO fluctuates around 2–4%, heavily influenced by market cycles. During bull markets, such lending rates can surge to 10%–20%, though they remain highly volatile and lack stability. In such high-volatility interest rate environments, Pendle can serve as a tool to lock in or redeem this portion of interest in advance. At this point, using Pendle to realize future yields upfront becomes a viable option.

RWA Market (Primarily U.S. Treasuries)

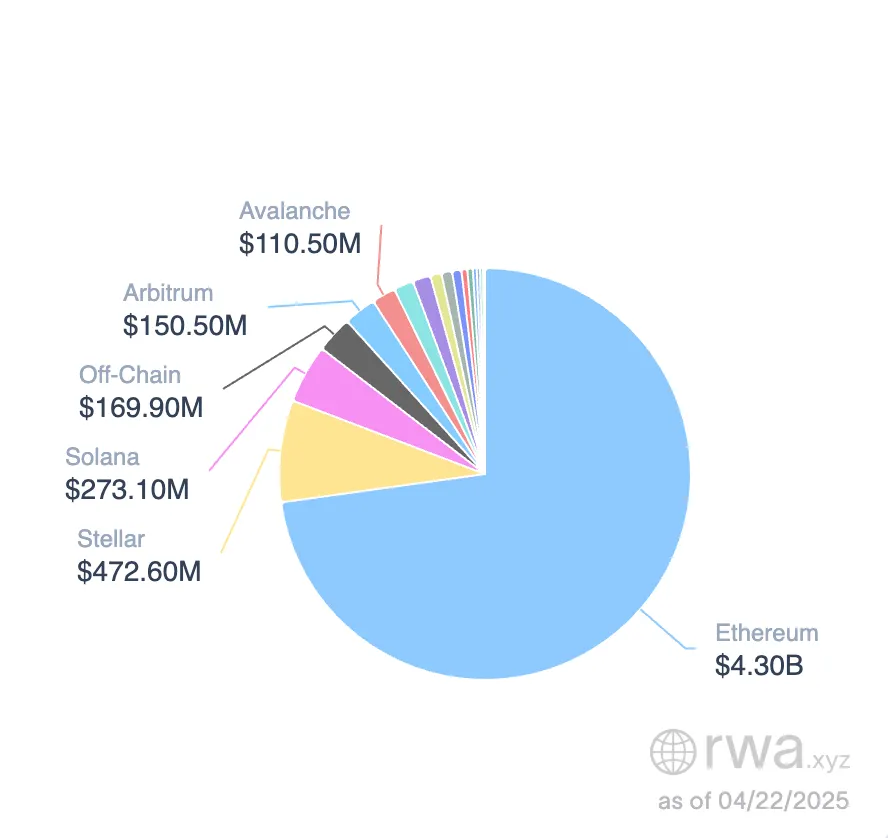

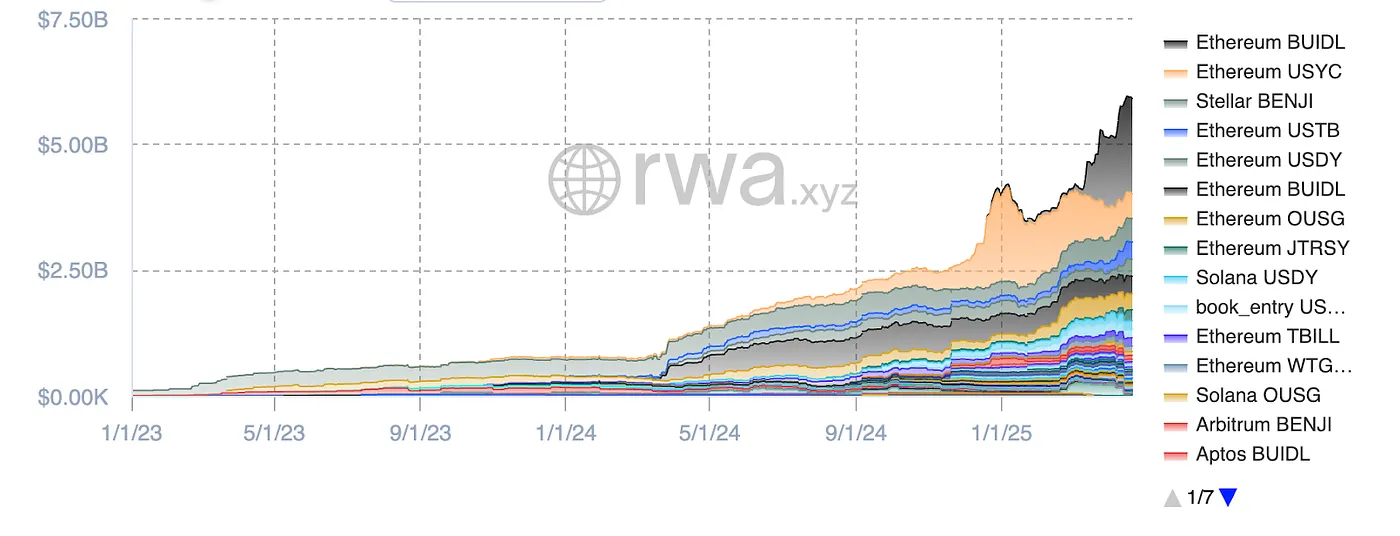

Opportunities in the RWA Stablecoin Market, Image Source: RWA.xyz

Currently, stablecoins backed by U.S. Treasuries are showing a steady growth trend, with the total market size reaching $5.9 billion. The Ethereum ecosystem dominates this sector, accounting for over 80% of the market share. In terms of categories, BlackRock’s BUILD holds the largest share of the Treasury-backed stablecoin market at 32% (around $1.9 billion). It is followed by Circle’s USYC (approximately $490 million) and Franklin Templeton’s BENJI.

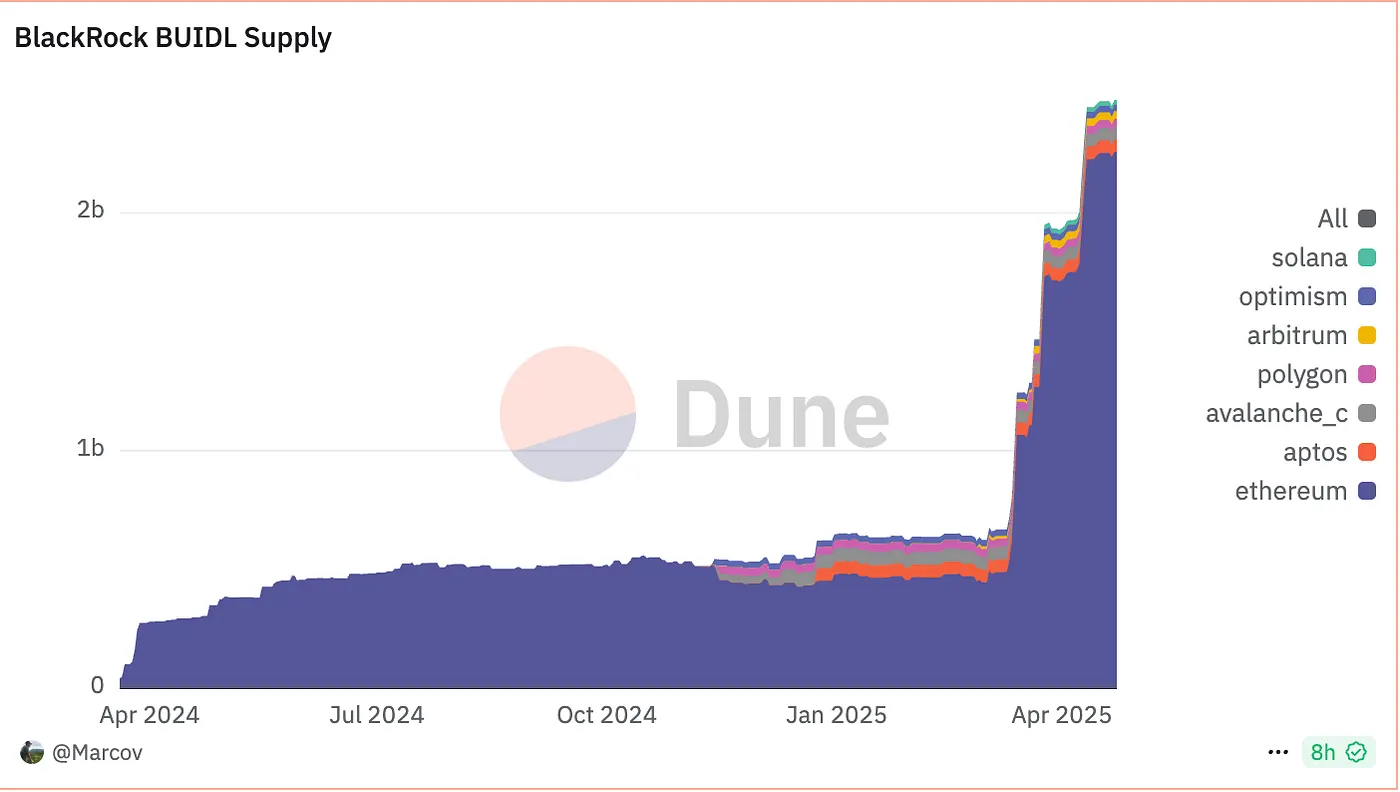

BUIDL Supply, source: Dune

Taking BUIDL as an example: although it is pegged to 1 USD, it is not essentially a stablecoin for everyday payments, but rather a fund share benchmarked against short-term U.S. Treasuries, cash, and overnight repo agreements. Users can subscribe using USDC/USD, with each BUIDL representing $1 of principal, while yields are distributed through a monthly rebase mechanism. Early participants included Anchorage Digital Bank NA, BitGo, Coinbase, and Fireblocks.

The supply of BUIDL has been growing rapidly, with a minimum subscription threshold of $5 million. As of May 1, 2025, a total of 48 clients had participated, pushing assets under management (AUM) to $2.47 billion. According to Ondo Finance, the product offers an annualized yield (APY) of around 4%, aligning with the prevailing U.S. Treasury rates for maturities of 3 to 6 months.

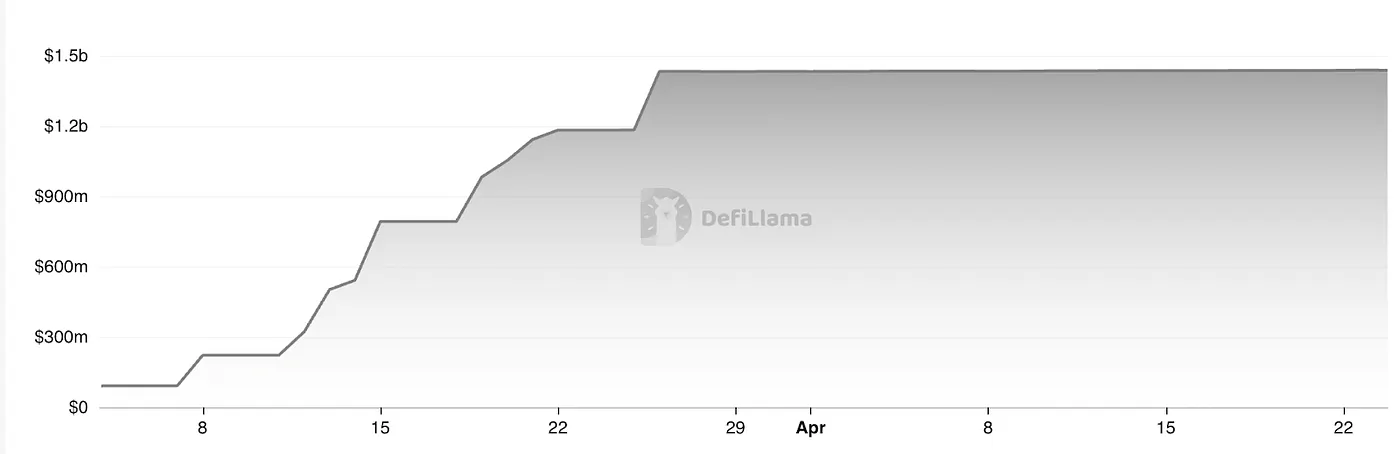

USDtb TVL, source: Defillama

Building on the existing money-market-style stablecoins, Ethena’s USDtb represents an innovative attempt. The product is constructed with the BUIDL tokenized fund as its underlying asset. Unlike Ondo’s OUSG and BlackRock’s BUIDL, USDtb enables free circulation. At present, it has reached an assets under management (AUM) of around $1.43 billion and has formed a deep partnership with Bybit, with overall market liquidity performing well.

Overall, the RWA-backed stablecoin market is expanding rapidly, with a total size of about $5.9 billion. Ethena’s USDtb offers a new reference point: if U.S. regulators eventually permit the “yield-distributing stablecoin” model, the market ceiling for such products could theoretically align with U.S. money market funds—reaching as high as $6 trillion.

In the short to medium term, however, U.S. Treasury yields face downward pressure. Since today’s stablecoin market is primarily rate-driven rather than payment-driven, money-market-based stablecoin strategies may face shrinking returns in the near term. Yet from a long-term perspective, this sector still holds strong growth potential.

The “Savings Rate” of Collateralized Stablecoins

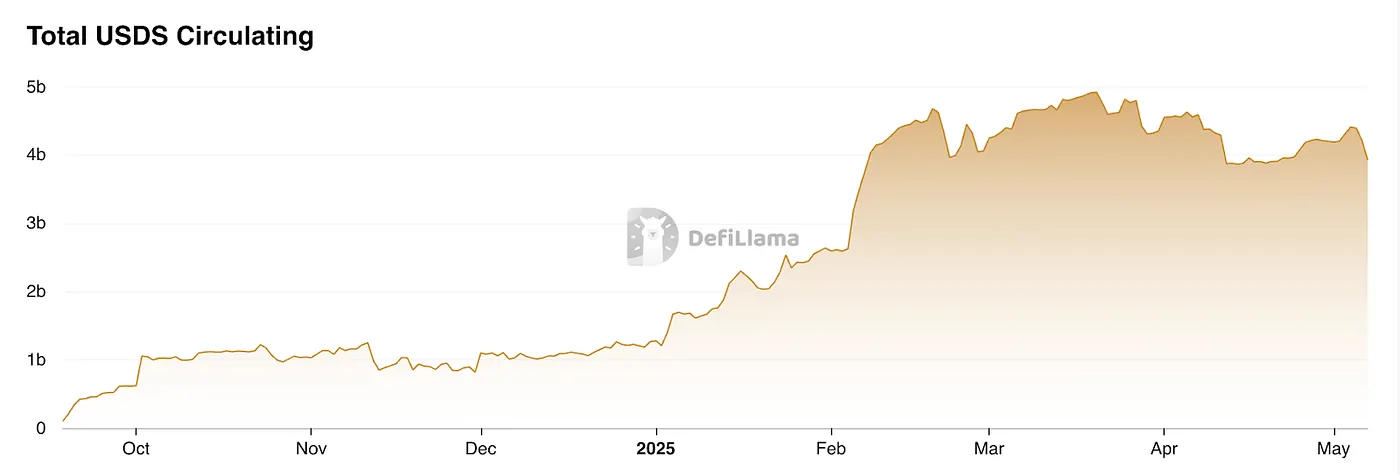

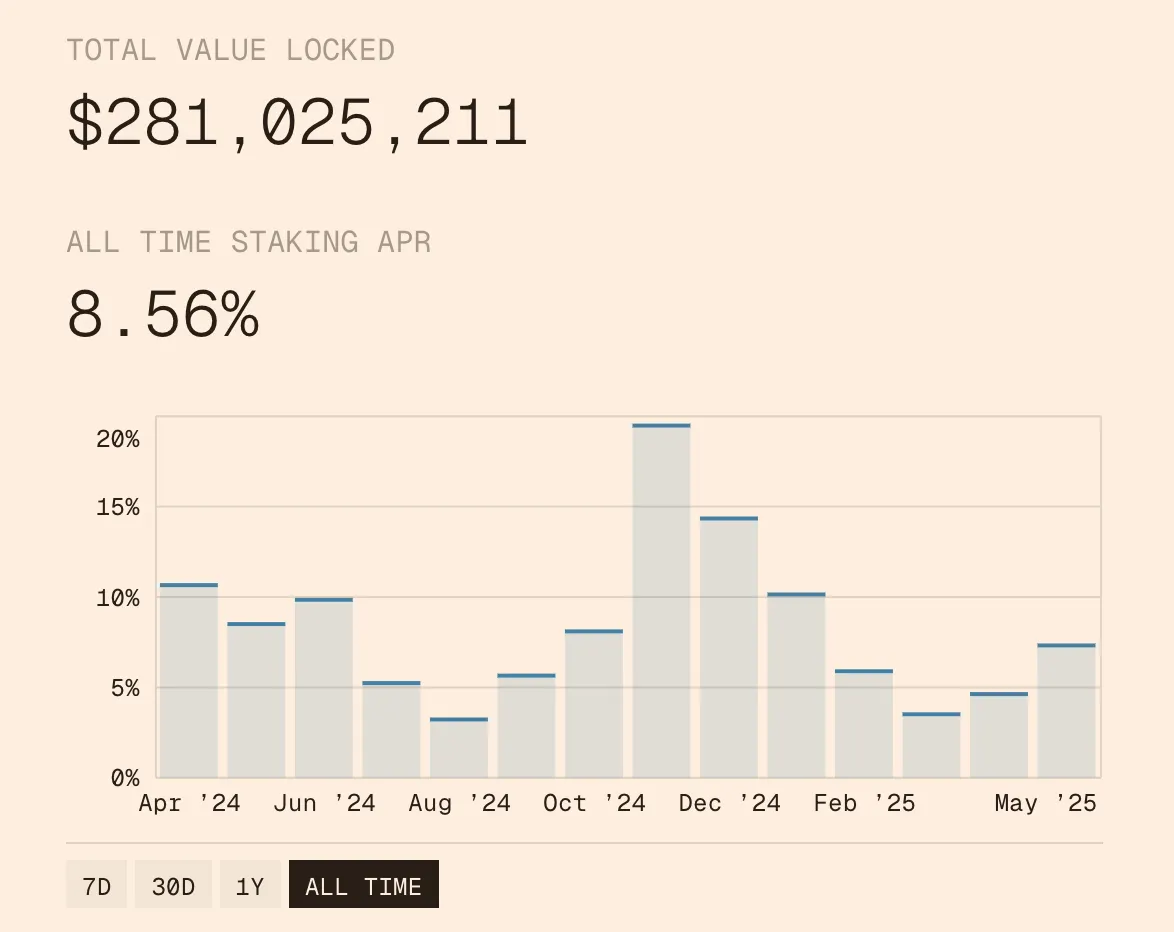

The DSR (Dai Savings Rate) was originally introduced by MakerDAO and has since evolved into the SSR (Stablecoin Savings Rate) module within Sky.money. This module allows USDS holders to earn a share of protocol revenue at an annualized rate. Interest accrues in real time per block, with no lock-up and no fees, enabling users to deposit and withdraw at any time.

The yield comes from profits generated by MakerDAO/Sky.money. To promote the broader adoption of USDS in DeFi, Sky.money has established an incentive mechanism that allocates part of protocol revenue to the USDS savings rate. Currently, this rate is around 4.5% APY.

USDS Growth, source: Defillama

Essentially, this represents a protocol dividend-style stablecoin model. During market downturns, Sky.money redirects profits—originally intended to support its native token—toward USDS adoption, which may weaken price support for the native token. In bullish conditions, however, moderately reallocating token revenue in exchange for overall protocol growth can help boost token value, making it a reasonable strategy. Because this model is deeply tied to the protocol itself, Sky.money must hold sufficient influence to truly drive USDS into becoming a widely used unit of account. This is both a highly ambitious and inherently challenging goal.

Derivatives Hedging + Staking Yields

The derivatives hedging rate (also known as the delta-neutral rate) is a yield source derived from the derivatives market. It works by simultaneously holding long and short positions to lock in directional price risk (Delta), while capturing profits from funding rates or the spread between futures and spot prices. In the derivatives market, perpetual futures are the primary instrument. There are several types of yields in this category:

Gate Ventures

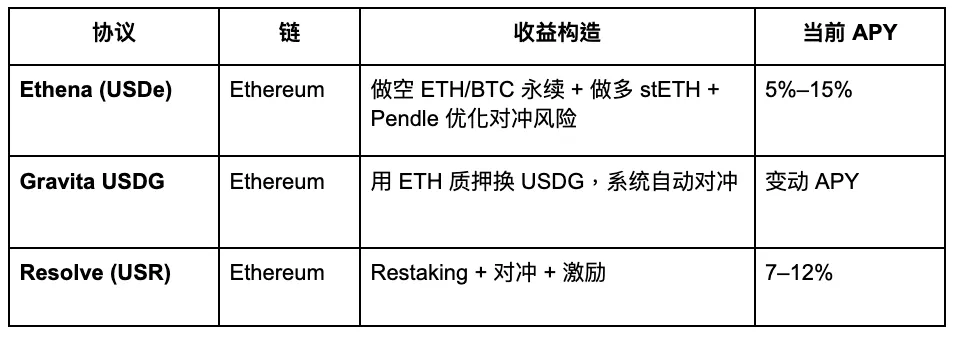

Some representative projects are as follows:

Gate Ventures

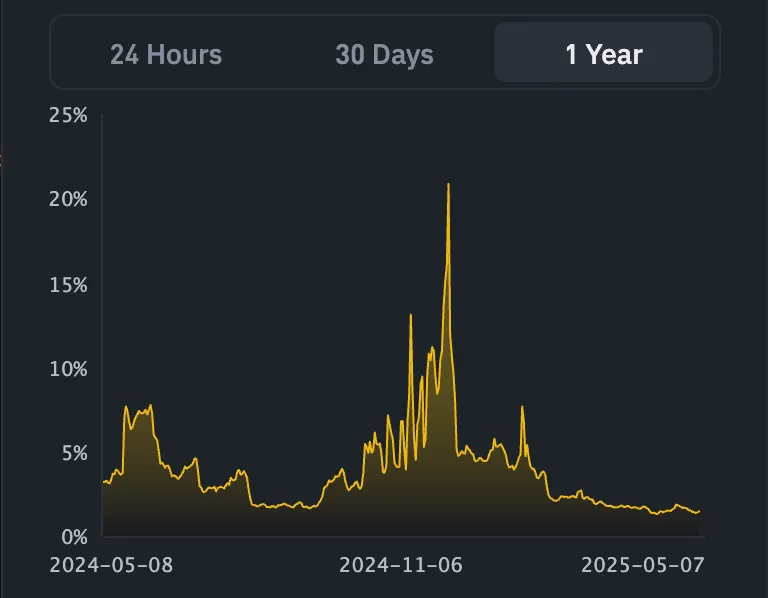

USDe APY, Source: Exponential.FI

USR APR, source: Resolve

The above shows the changes in stablecoin interest rates for USDe and USR. Overall, as the first delta-neutral stablecoin, USDe set the benchmark, while USR has followed as a competitor. Its current promotion strategy is to attract user deposits with a higher interest rate, though in essence, it does not differ significantly from Ethena.

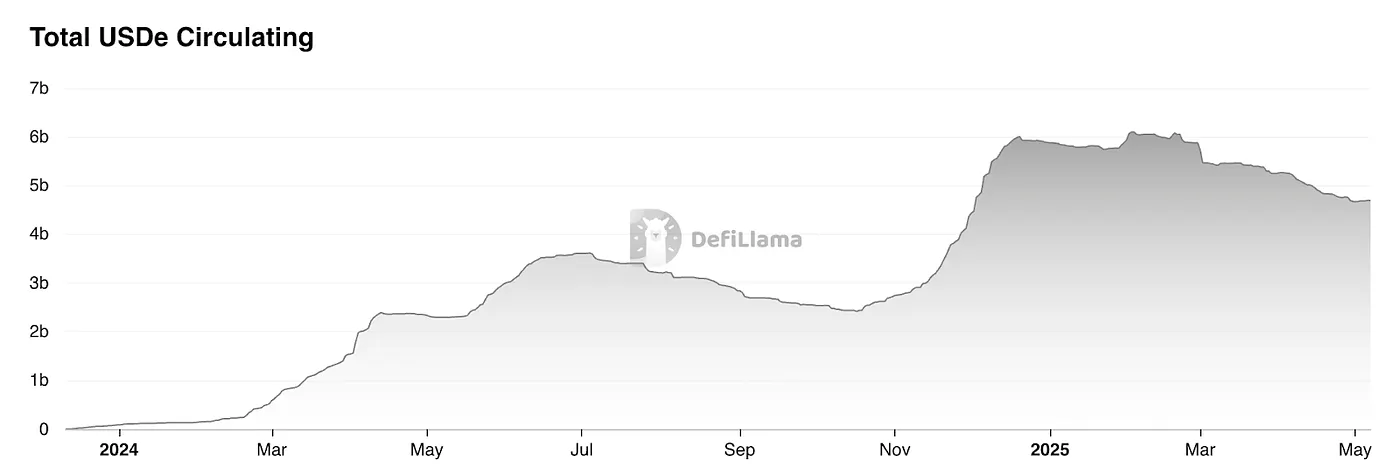

USDe TVL, source: Defillama

According to DefiLlama data, the market capitalization of Ethena’s stablecoin has declined significantly following its airdrop, falling about 20% from its peak. This drop is mainly driven by the decrease in USDe yields. In addition, stablecoins currently face a broader “financial Lego” dilemma—namely, the lack of rigid real-world demand. In essence, many of these products function more like fund structures designed to capture funding rate arbitrage.

The minting process of funding-rate-based stablecoins (Δ-neutral stablecoins) is as follows:

Purchase an equivalent amount of spot assets (or LST).

Open a short position of the same notional value in the perpetual futures market.

Thus, minting 1 USD worth of stablecoin ≈ 1 USD spot + 1 USD notional short position, which means that the theoretical minting capacity is constrained by the existing open interest (OI) in the perpetual futures market.

Ethereum OI, source: Coinglass

According to statistics from Coinglass, the total ETH open interest (OI) across major exchanges is currently around $20 billion. Based on conservative estimates, the market cap ceiling for USDe is approximately $4 billion.

All tokens’ OI, source: Coinglass

If we take into account the total OI across the entire network, the market size for funding-rate hedging strategies is about $120 billion. Conservatively, this type of strategy could capture around 20% of the market share, or roughly $24 billion.

In other words, the conservatively estimated addressable market for the entire funding-rate hedging strategy sector is $24 billion. Based on this, for USDe, which focuses primarily on the ETH market, the potential market size is approximately $4–8 billion. At present, USDe’s outstanding supply is about $4.6 billion and trending downward, suggesting that its growth is already approaching the upper limit, with a clear ceiling in sight.

Strategy Aggregation Vaults

For example, Idle Best-Yield has deployed an automated strategy system on Ethereum and Polygon that dynamically adjusts positions based on on-chain arbitrage opportunities to maximize stablecoin yields. Similarly, Hyperliquid’s HLP can also be seen as a strategy-based stablecoin yield pool, with its returns mainly derived from acting as the counterparty to retail traders’ positions. While these multi-strategy models can deliver higher returns, they also come with significantly higher risk exposure.

Binance Launches LDUSDT

We must always approach this type of stablecoin with caution, as it essentially resembles a subscription share of a hedge fund. As Binance explains in its introduction to LDUSDT, it is not a stablecoin but rather a new type of margin asset designed for users subscribed to the Simple Earn USDT flexible savings product. LDUSDT is a wrapped form of USDT, which can serve both as a margin collateral asset for contracts and as a way to earn the annualized interest from Binance Simple Earn. Therefore, its underlying yield is dependent on the lending market within Binance’s Simple Earn module.

Simple earn APR, source: Binance

The strategy-based stablecoins represented by Ethena’s USDe may be considered an innovative form. Overall, the rise of strategy-based stablecoins reflects a shift toward conservatism in the crypto market, but it can also be seen as progress. Unlike the previous cycle of stablecoins that relied on subsidies to drive growth, today’s stablecoins are more dependent on diversified, organic strategies that generate real yield, giving them stronger sustainability. However, once points or token airdrop subsidies are stripped away, their annualized yields show no clear advantage compared to U.S. Treasuries.

At the same time, the synergies within the DeFi ecosystem have not yet been fully unleashed, leaving stablecoins still largely confined to “financial Lego” internal use cases rather than driving real large-scale adoption. Getting exchanges to list such synthetic stablecoins is an important step toward broader Web3 adoption. Currently, Ethena is advancing relatively quickly in this area, with Bybit and Bitget already listing its trading pairs, and Gate having entered into a strategic partnership with Ethena. Still, the results remain underwhelming, as the 24-hour trading volume of USDe/USDT across the entire market is still under $100 million.

Stablecoin Project Overview

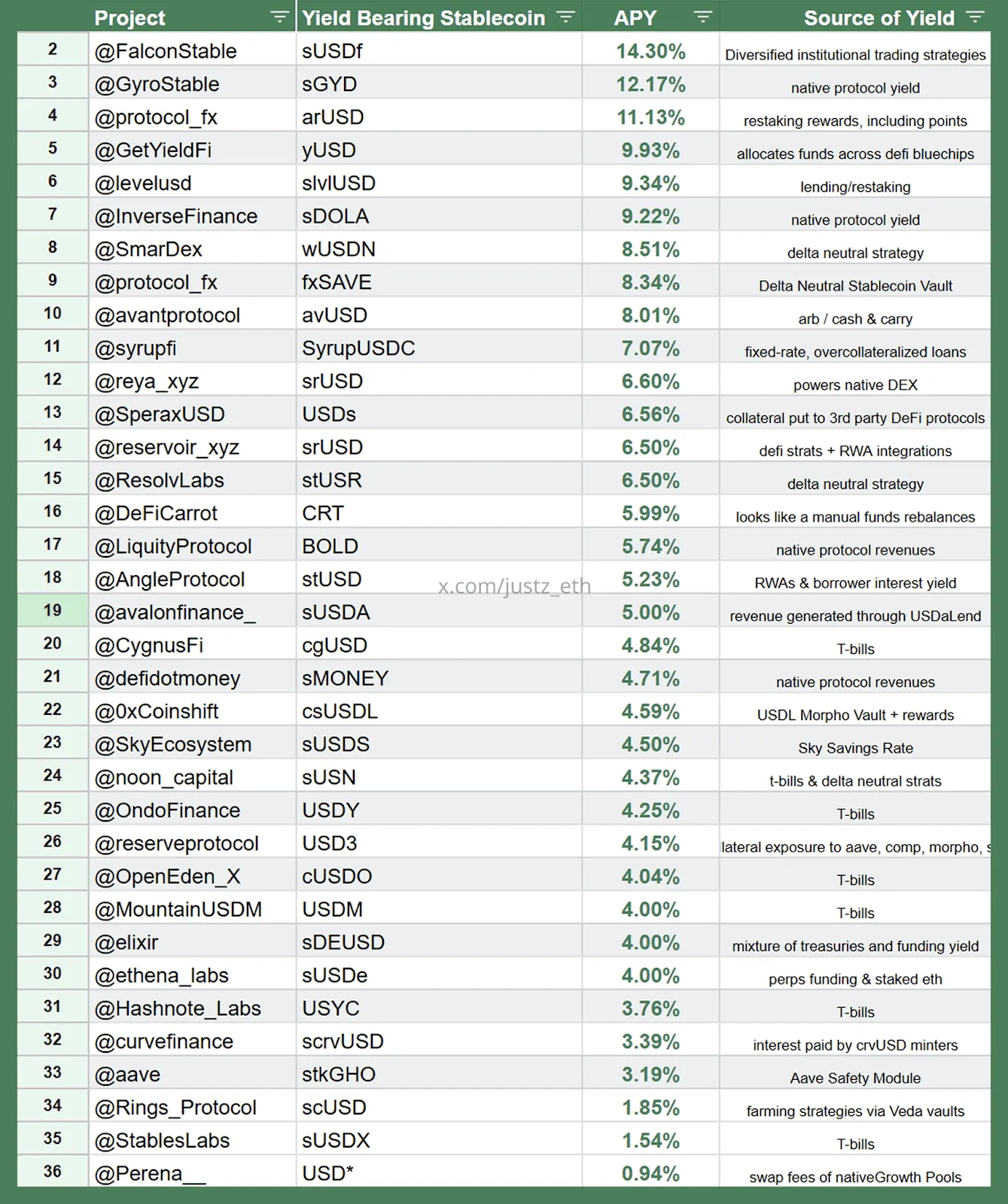

Strategy-backed Synthetic Stablecoins Landscape, source:justz_eth

The above shows more strategy-based synthetic stablecoins, and the chart also specifies the yield source strategy corresponding to each stablecoin.

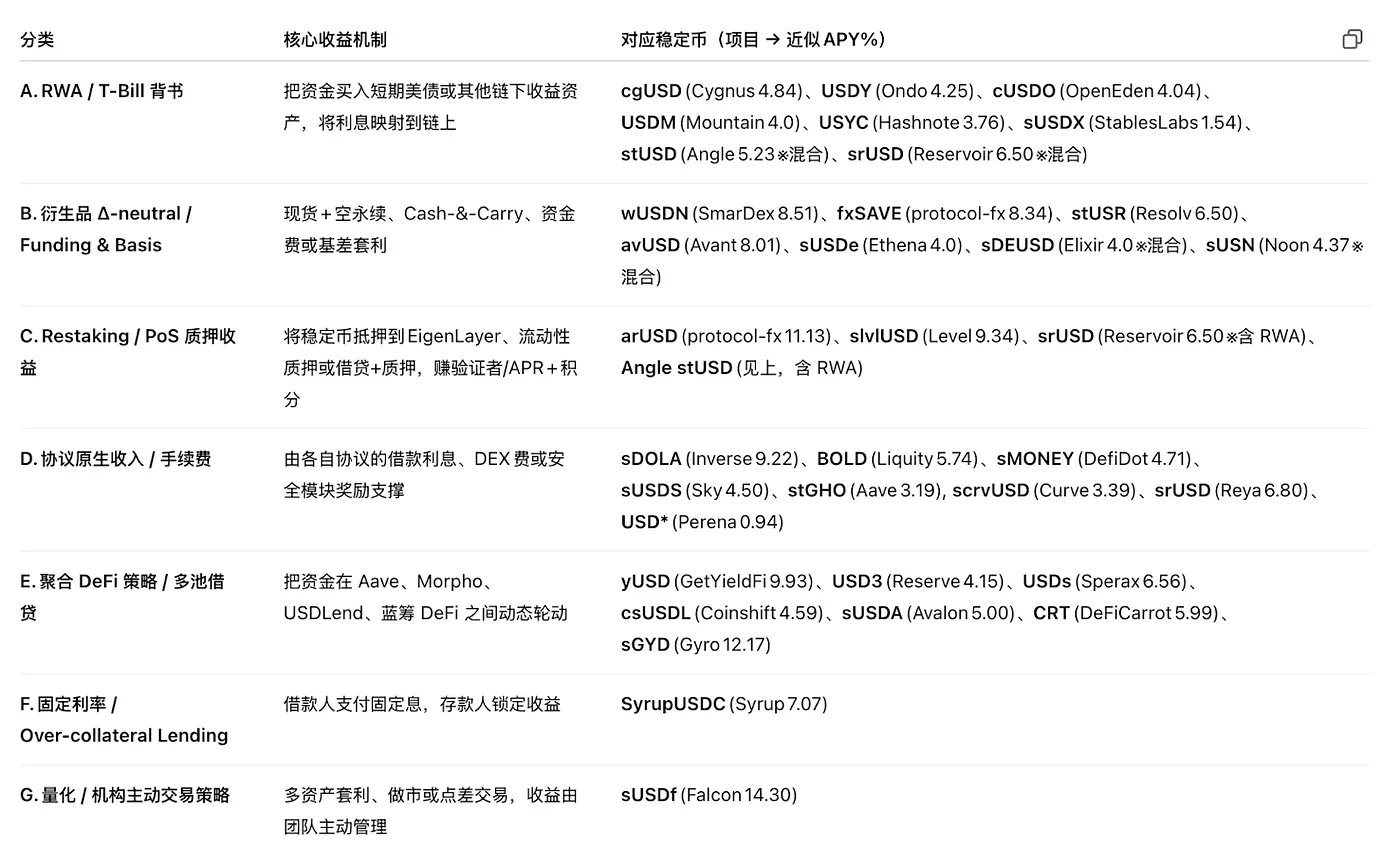

Strategy Classification, source:justz_eth

Some of the popular stablecoin projects in the current market derive their underlying synthetic asset yields from the strategies we mentioned earlier. However, it should be noted that many projects may have inflated TVL figures, with some even having special arrangements with large holders. Readers should therefore approach these numbers with caution. At their core, these stablecoins are closer to hedge fund share subscriptions, which also exposes them to the legal risk of being classified as securities.

In terms of market share, the U.S. Treasury–backed stablecoin sector is relatively larger in scale. The successful implementation of large-scale adoption in this track relies heavily on supportive regulation and integration with the banking system, which is why we hold a relatively more favorable outlook on these projects. Other strategies—such as lending rates, restaking yields, risk-free rates from derivatives, and protocol revenue—each face clear ceilings, so participation should be approached with caution.

New Approaches to Interest Rates

Below are some of our ideas, provided only as references for entrepreneurs:

First is new ways to utilize assets. As a key bridge between TradFi and Web3, BTC carries a market capitalization in the trillions of dollars. If BTC-Fi could be leveraged to introduce a base interest rate into stablecoins and build a BTC-ecosystem-based stablecoin system, the difficulty of promotion might be lower than in other blockchain ecosystems. The challenge, however, lies in the lack of underlying infrastructure within BTC itself. One possible entry point could be from off-chain, such as initiating contract rate arbitrage strategies around BTC, but the overall logic still falls within the scope of strategy-based hedge funds.

Second is new applications of strategies. In theory, any arbitrage strategy could serve as a yield source for stablecoins. For instance, on-chain MEV, implied vs. realized volatility spreads (IV-RV), cross-maturity volatility arbitrage, GameFi yields, or even security fees provided by EigenLayer AVS and revenues from DePIN devices could all be incorporated into a stablecoin’s interest mechanism, thereby giving rise to new stablecoin interest rate models.

That said, these still belong to the category of strategy-based synthetic stablecoins, rather than traditional stablecoins backed by real-world assets. Their market capacity is constrained by the feasible space of the strategies themselves—namely, the size of the underlying markets they depend on. At present, most of these related markets remain relatively small. In the long run, however, as DeFi continues to expand, this track holds strong growth potential—particularly since many of these strategies are highly crypto-native, making them more responsive to on-chain market dynamics.

Pendle: The Beneficiary of the Stablecoin Wars

Fixed interest is an innovative yield mechanism designed to provide users with predictable, fixed returns, similar to zero-coupon bonds in traditional finance. In traditional markets, zero-coupon bonds are issued at a discount to face value and redeemed at par upon maturity, without paying interest during the holding period. The investor’s return comes from the difference between the purchase price and the redemption amount. In DeFi, a similar mechanism has been introduced by Pendle, which tokenizes the future yield of yield-bearing assets, enabling users to:

Lock in fixed returns: By purchasing tokens that represent the principal and holding them until maturity, users can secure fixed income.

Speculate on yields: By purchasing tokens that represent future yields, users can bet on changes in interest rates.

Improve capital efficiency: By selling future yields for immediate liquidity while retaining ownership of the principal.

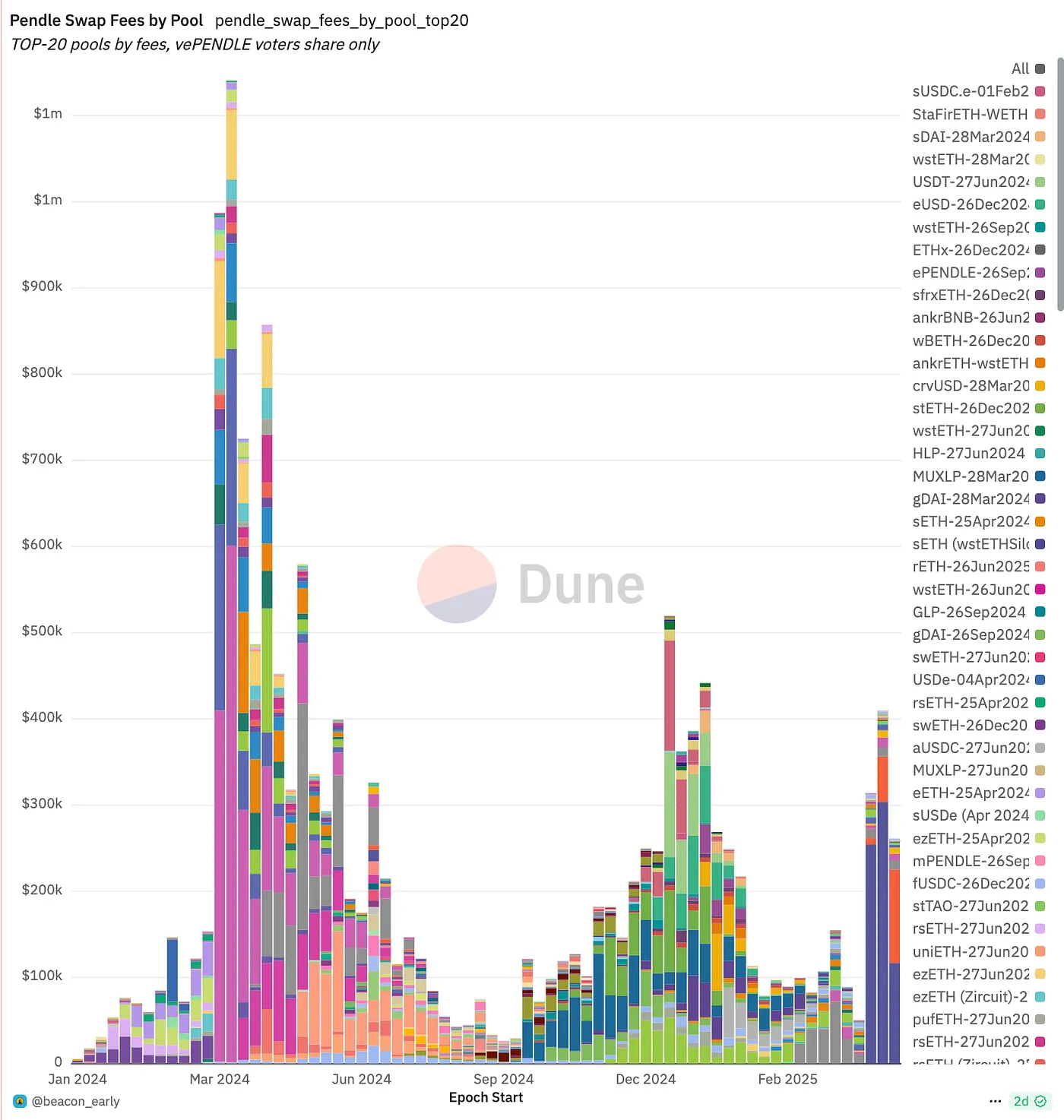

Pendle Snapshot, source:pendle

Pendle is a DeFi protocol focused on yield tokenization, allowing users to split yield-bearing assets into PT (Principal Token) and YT (Yield Token), which can then be traded on its platform. Essentially, Pendle has built a trading market around interest rates themselves, providing a hedging mechanism for the yield strategies underpinning stablecoins, thereby enabling the creation of fixed interest rates.

During the previous LRT boom, Pendle’s token price once saw a sharp decline following the launch of EigenLayer’s token. However, with the rise of strategy-based stablecoins, Pendle’s TVL has experienced explosive growth. It is gradually establishing itself as the core “interest rate exchange layer” for such assets: stablecoin issuers can use Pendle to sell future yields upfront in order to hedge risk, while speculators and asset managers can buy or market-make these yield streams. With the launch of more Δ-neutral and RWA hybrid yield stablecoins, Pendle’s TVL, trading volume, fee revenue, and vePENDLE ecosystem have all been rising in tandem. At present, it has established a near-monopolistic leading position within this sector.

Source:

- https://defillama.com/yields/pool/13392973-be6e-4b2f-bce9-4f7dd53d1c3a

- https://ondo.finance/ousg

- https://defillama.com/yields/pool/c8a24fee-ec00-4f38-86c0-9f6daebc4225

Disclaimer:

This content does not constitute any offer, solicitation, or recommendation. You should always seek independent professional advice before making any investment decisions. Please note that Gate and/or Gate Ventures may restrict or prohibit some or all services for users from restricted regions. Please read the applicable user agreement for more information.

About Gate Ventures

Gate Ventures is the venture capital arm of Gate, focusing on investments in decentralized infrastructure, ecosystems, and applications that will reshape the world in the Web 3.0 era. Gate Ventures partners with global industry leaders to empower teams and startups with innovative vision and capabilities, redefining the way society and finance interact.

Website: https://www.gate.com/ventures

Thanks for your attention.

Share

Content

TL;DR

Strategy-Based Stablecoins

On-Chain Lending Market

RWA Market (Primarily U.S. Treasuries)

The “Savings Rate” of Collateralized Stablecoins

Derivatives Hedging + Staking Yields

Binance Launches LDUSDT

Stablecoin Project Overview

New Approaches to Interest Rates

Pendle: The Beneficiary of the Stablecoin Wars

About Gate Ventures